Chart of the Week

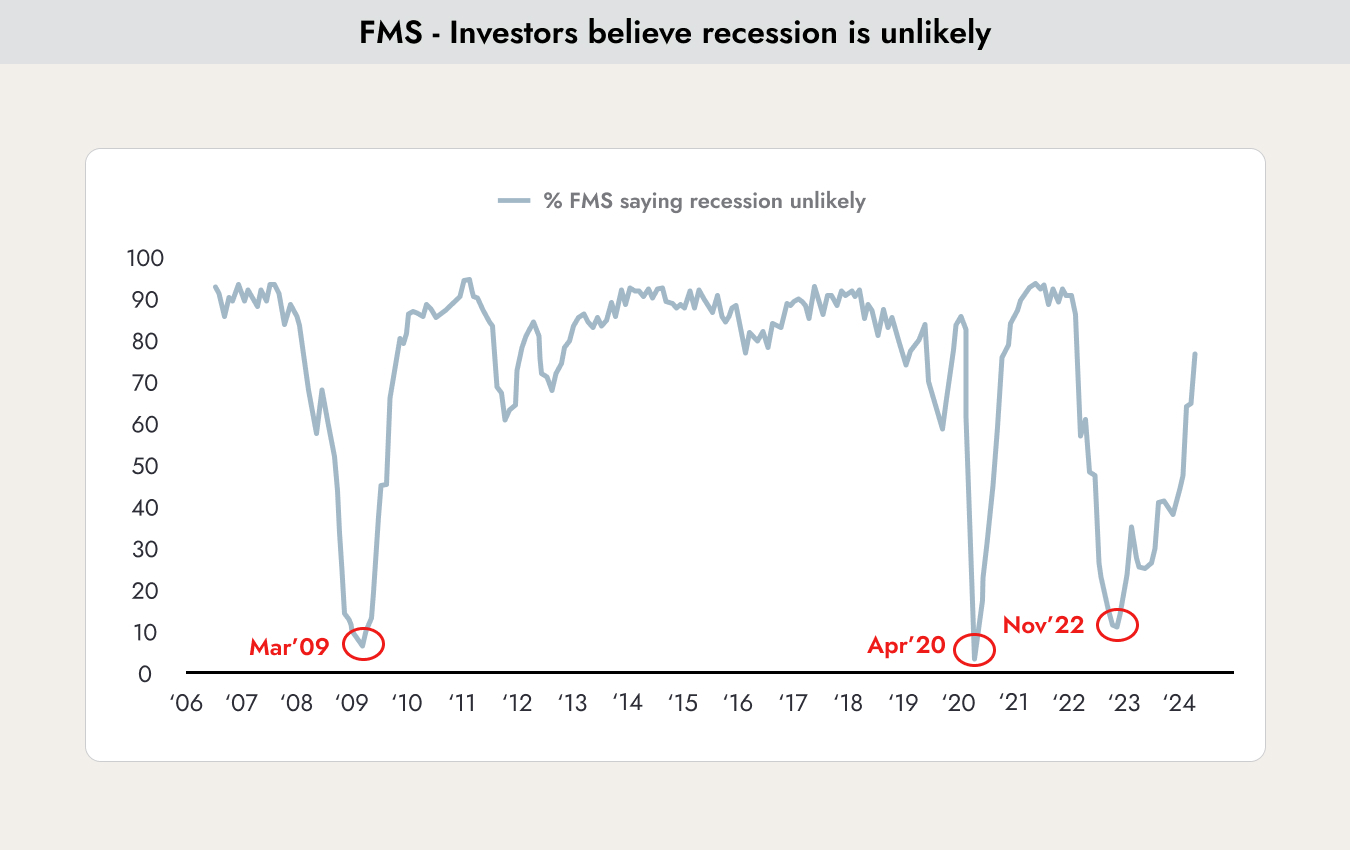

The chart shows a Bank of America survey of the largest institutional investors on whether a recession in the next 12 months is unlikely. In November 2022, 90% expected a recession, while now only 10% do.

Why This Matters

The chart perfectly illustrates the shift in market sentiment. For most investors, the situation seems clear, and despite the historically sharp interest rate hikes of recent years, they do not expect a recession.

We still cannot share this optimistic view. Since the existence of the US Federal Reserve, there have been 15 interest rate hiking cycles, and 14 of them were followed by a recession. We consider the sentiment among most investors to be overly optimistic.

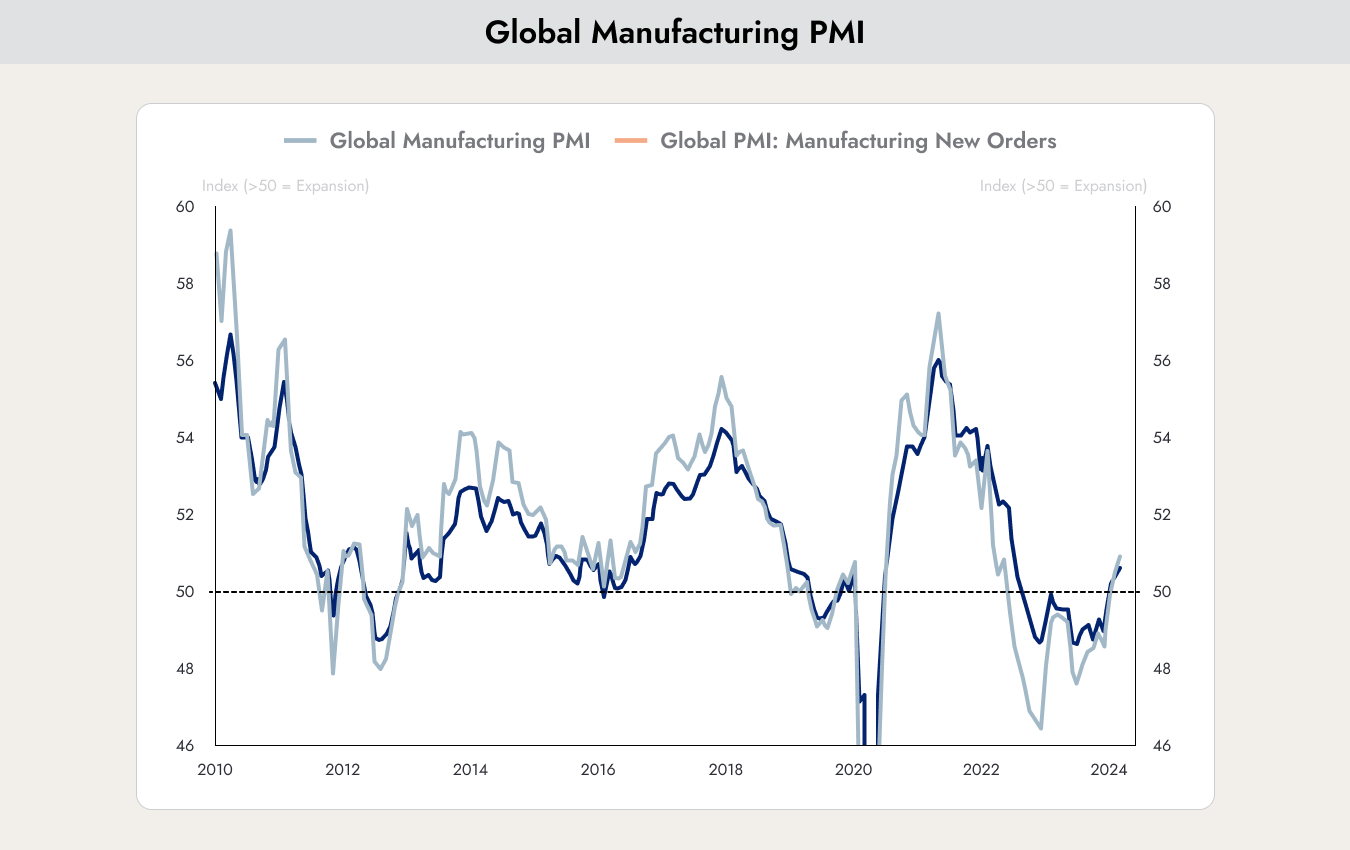

However, our view could also change soon. The following chart could make us reconsider:

The chart shows the Purchasing Managers’ Index (PMI) for the manufacturing sector (dark blue) and new orders (light blue). A reading below 50 indicates a contracting economy, while a reading above 50 indicates an expanding economy.

In 2024, the global economy returned to expansion. The recession in the manufacturing sector therefore appears to be over.

Since the increasingly important services sector, mainly driven by the artificial intelligence theme, was never in a recession, many people did not notice the downturn in industry.

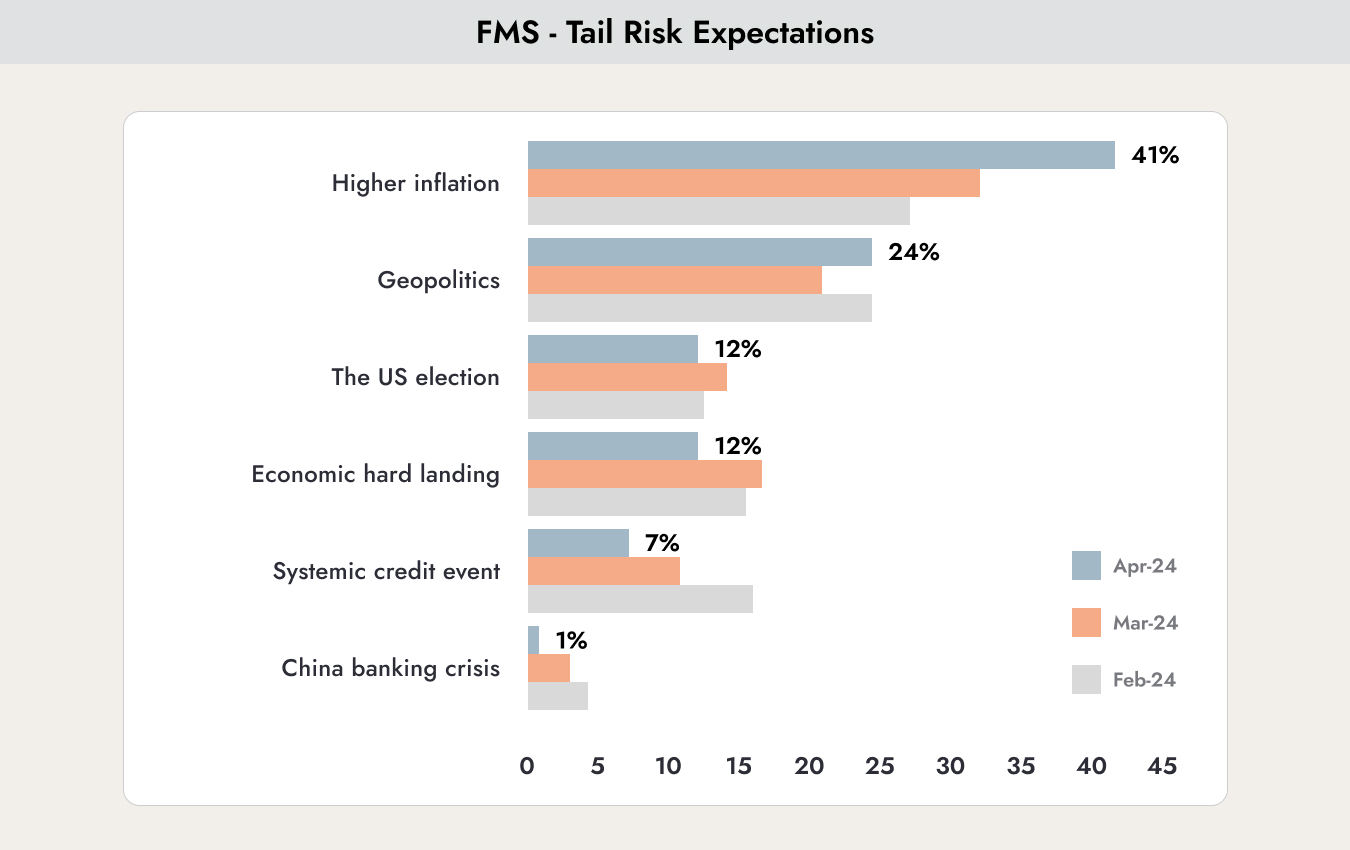

The chart shows a Bank of America survey of the largest institutional investors on where they see the biggest risks over the next 12 months. Fears of a recession (economic hard landing) have declined significantly. Instead, many are now concerned that inflation data could surprise to the upside, mainly due to geopolitical tensions and rising oil prices.

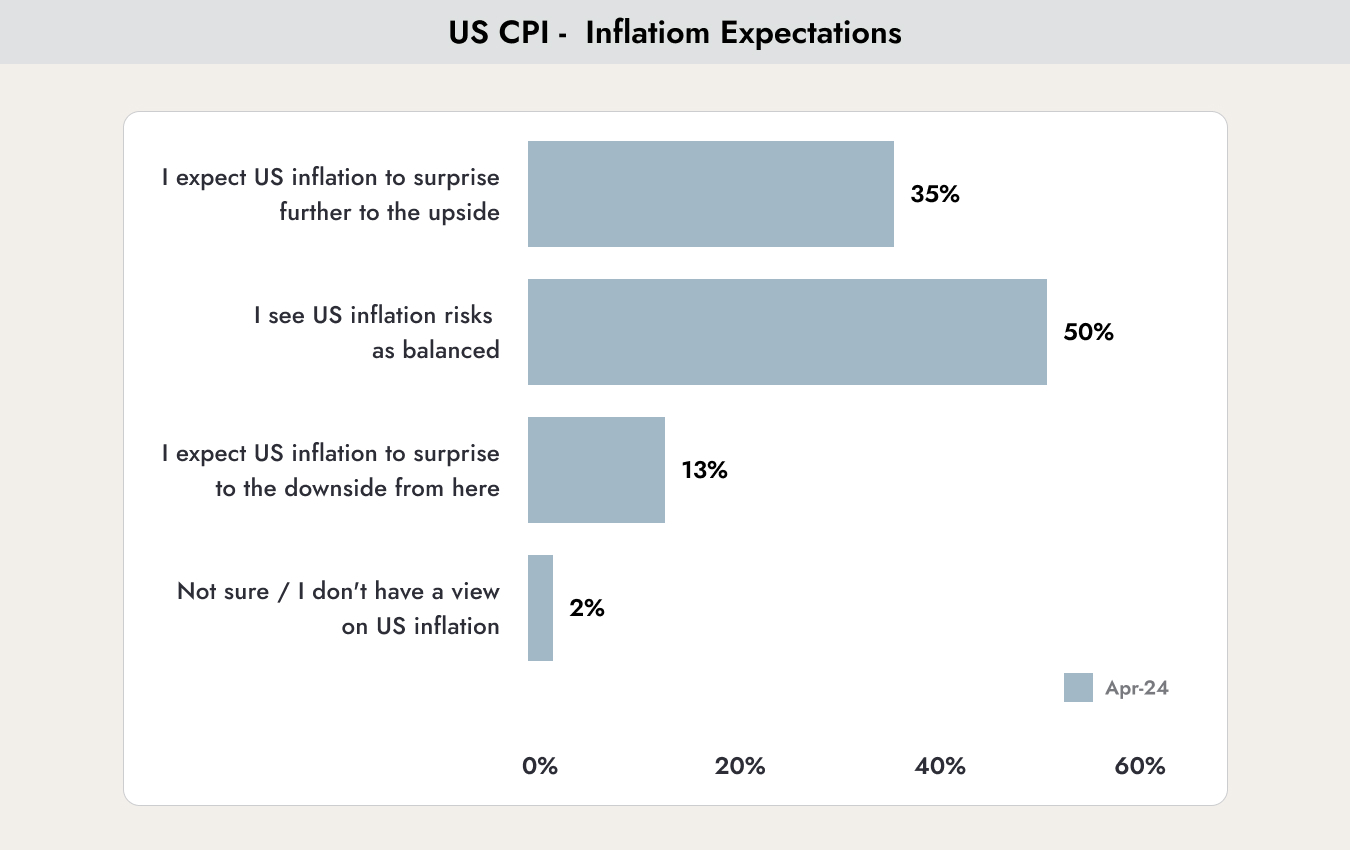

This chart also shows a Bank of America survey, but this time exclusively among institutional bond investors. From a positive perspective, more than 60% of investors expect inflation to remain stable or decline. However, 35% still expect higher inflation. At the beginning of the year, this figure was still close to 0%.

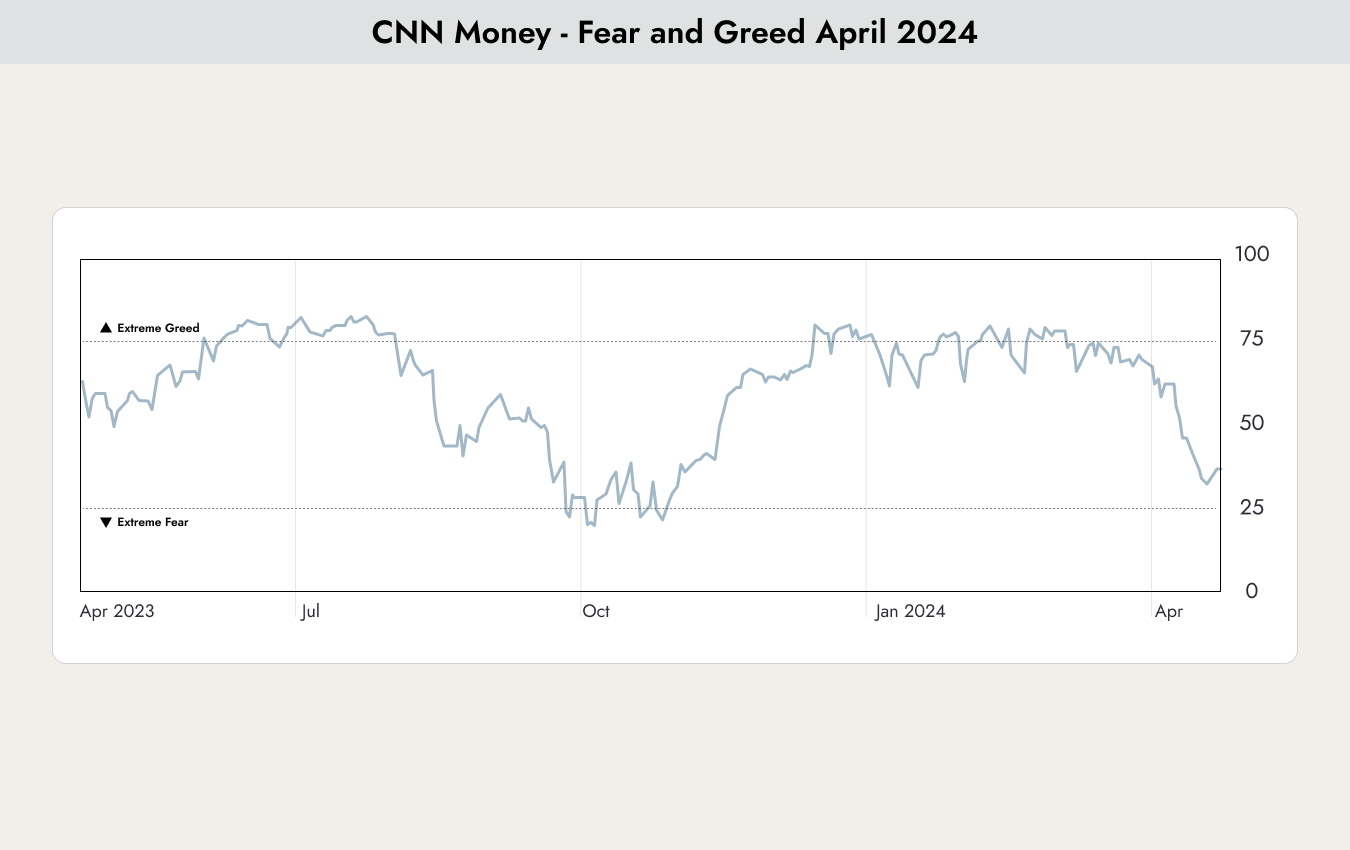

The chart shows how euphoric sentiment among retail investors had become. From December 2023 to March 2024, sentiment was at extremely high levels. Since April, the mood has shifted. The trigger was disappointment in some of investors’ favorite stocks, such as Tesla and Nvidia, which have declined sharply in recent weeks.

But that was only the trigger. We had already been warning about a correction for several weeks. With the shift in interest rate expectations, it was only a matter of time before prices adjusted to reality. We also believe that the correction is not yet over.

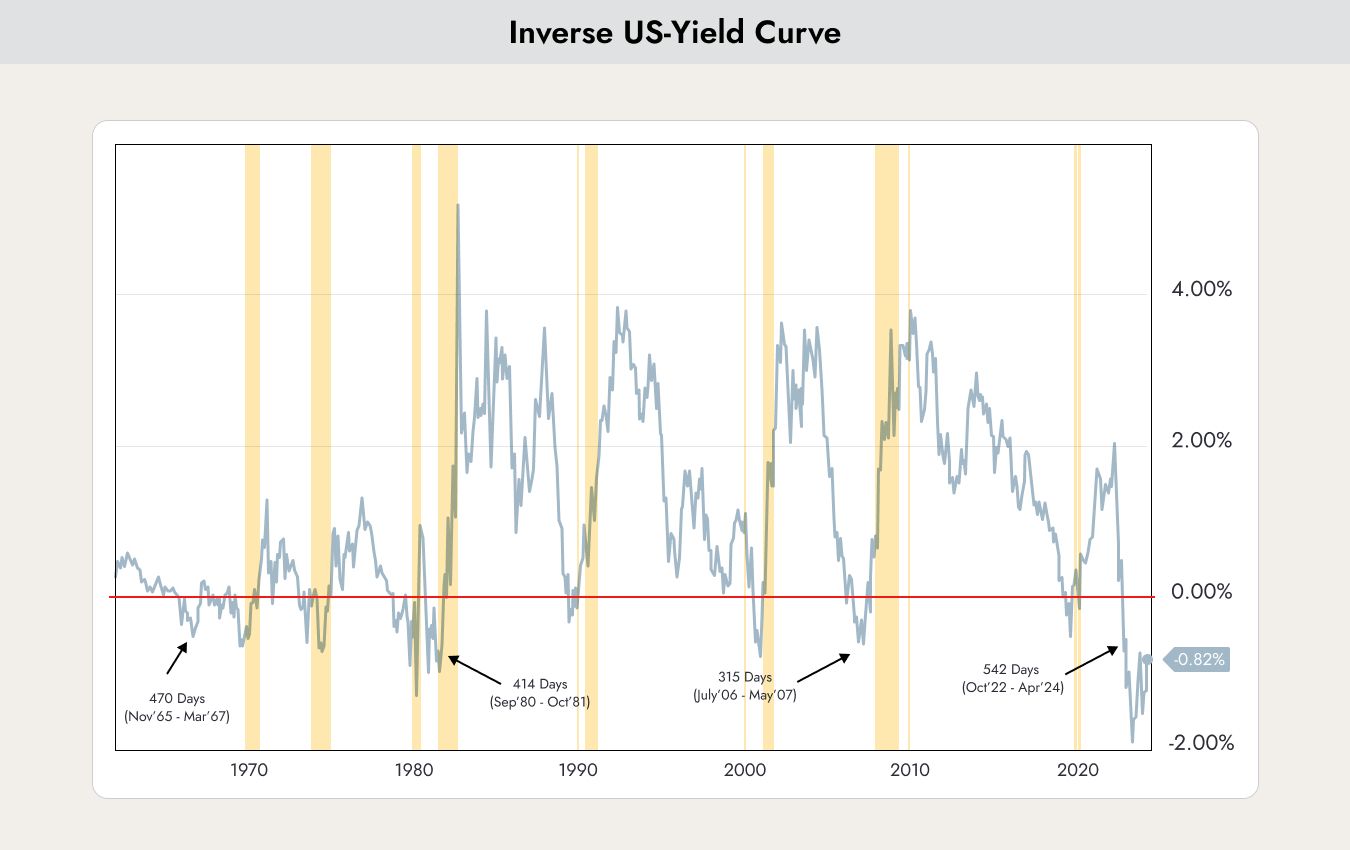

What continues to concern us is the inverted yield curve:

The chart shows the spread between 10-year US Treasury bonds and 2-year US Treasury bonds. Normally, long-term interest rates are higher than short-term rates because there is more uncertainty over longer periods. Currently, however, short-term interest rates are higher, which is known as an inverted yield curve.

In the past, this has always been a sign that a recession is coming. Although equity investors are very optimistic and are dismissing the possibility of a recession, bond investors still appear to be expecting one. Historically, bond investors have usually been right. They are largely long-term institutional investors, such as pension funds, who are not driven by sentiment in the media.

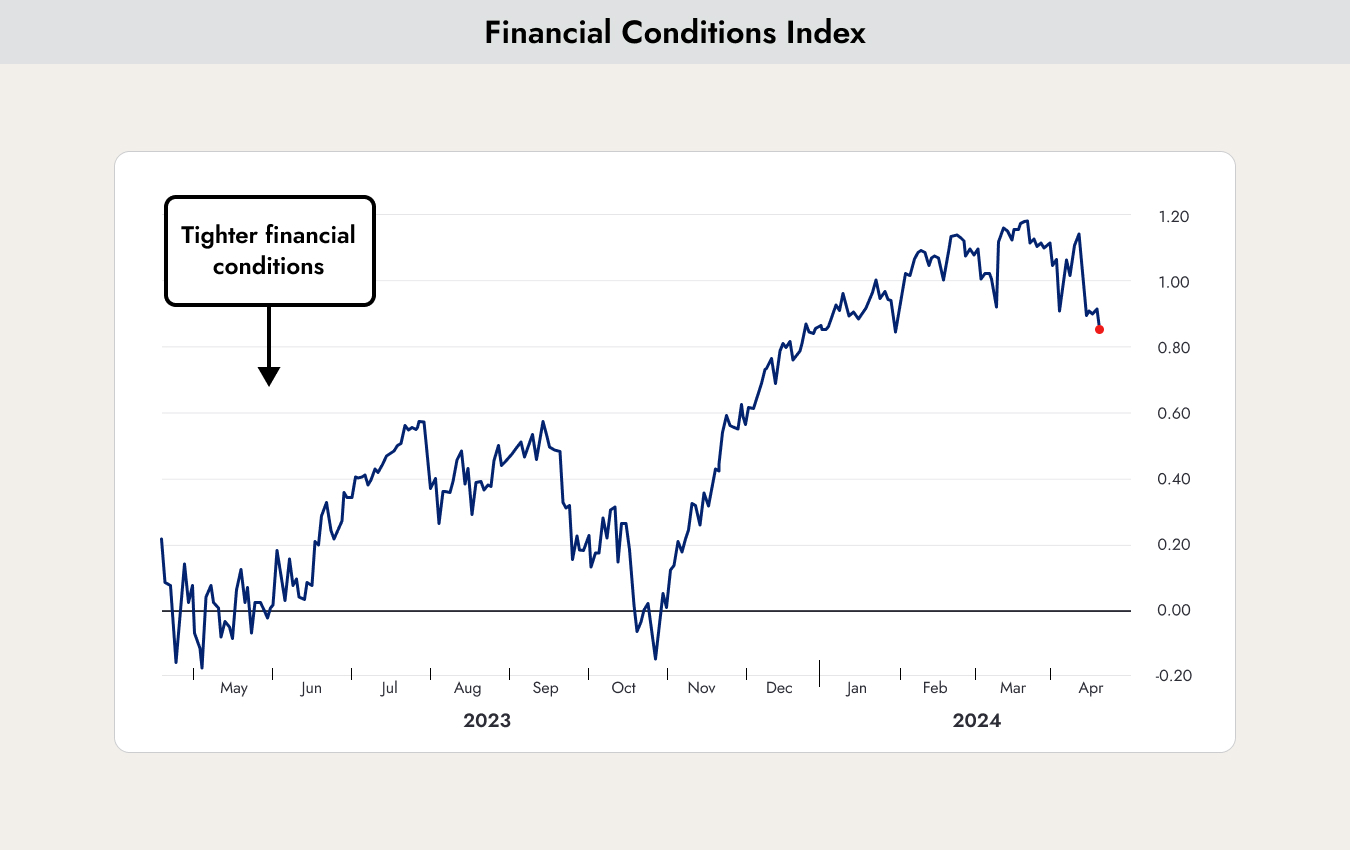

For the economy, what matters most is how easily businesses can access credit to finance their operations. Since November 2023, conditions have improved significantly for many companies:

Bloomberg calculates an index that shows how easily companies can obtain financing. One of the most important factors is, of course, the level of interest rates, but other indicators are also included in the calculation. The most closely watched index in this area is the one published by the Chicago Federal Reserve, which incorporates 105 data points.

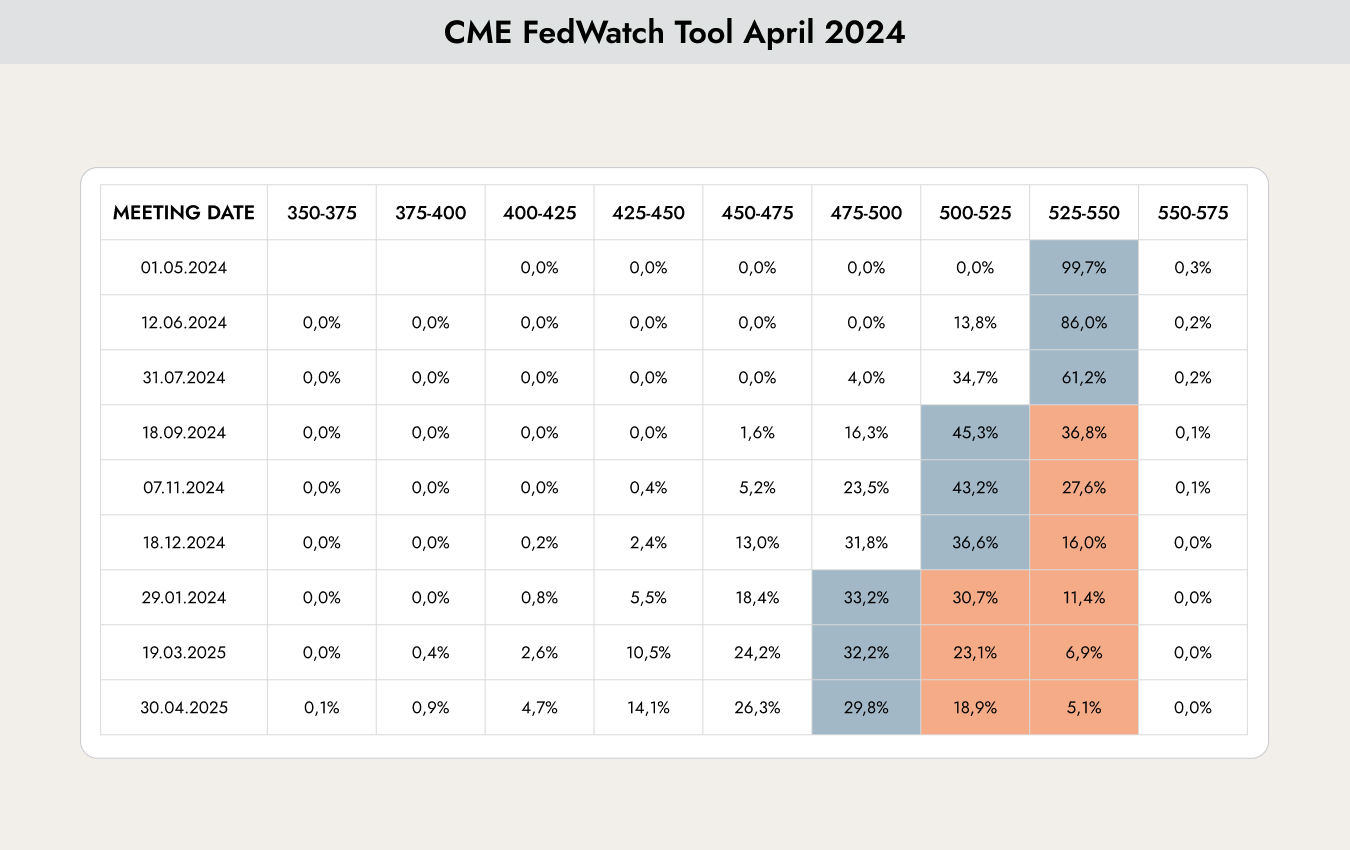

A higher value in the index means easier financing conditions. Since March, the index has started to decline again. At the beginning of the year, markets were expecting seven interest rate cuts, while now only two are expected:

The chart shows the probabilities investors assign to future interest rate decisions by the US Federal Reserve. At the Fed’s next meeting on May 1, investors see a 99.7% probability that interest rates will remain unchanged. However, markets are currently expecting rate cuts of 0.25% each in September 2024 and January 2025.

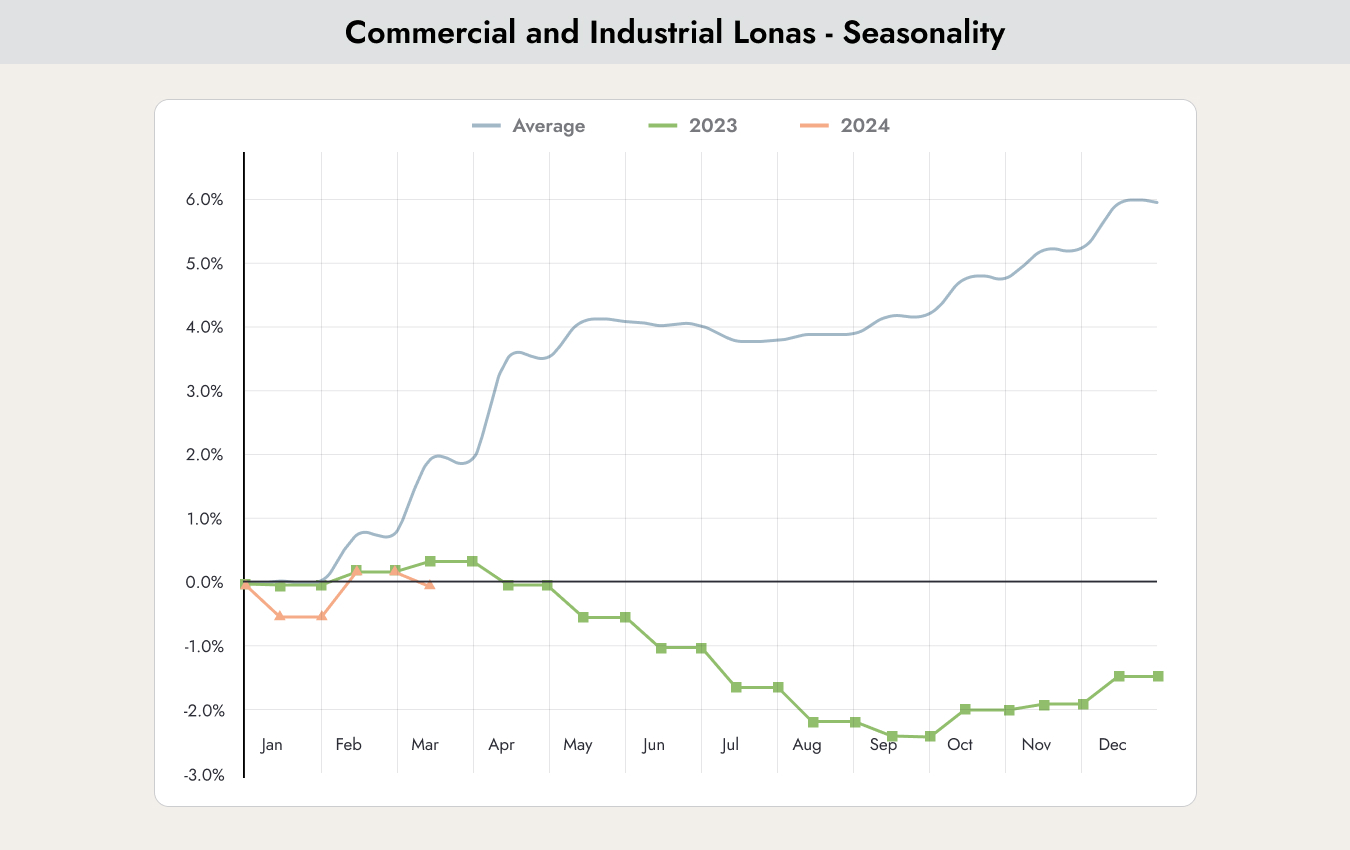

Today’s investments are tomorrow’s profits. In addition to the inverted yield curve, what concerns us is that although financing conditions improved over the past year, companies have not increased investments and have shown very little demand for credit.

The chart shows demand for corporate loans in the United States. The blue line represents the average trend in demand over the past 20 years. In 2023, demand for corporate loans declined, and 2024 appears to be heading in the same direction.

So far, companies do not seem to believe in a strong economic outlook and remain cautious about making additional investments. Only when this changes will we reconsider our currently very cautious and conservative investment strategy.

.webp)

.jpeg)

.jpeg)

.svg)