Long-term wealth planning in Zumikon is the process of coordinating investments, estate structures, tax strategy, and family governance to secure financial stability across multiple generations. This is not simply about accumulating assets. It is about building a framework that prevents wealth from eroding as it passes from one generation to the next. Nearly 70% of wealthy families lose their fortunes by the second generation, primarily because planning is fragmented rather than integrated. In Zumikon, where families often hold significant intergenerational assets, Swiss legal structures such as the Familienstiftung (family foundation) and the Erbvertrag (inheritance contract) play a central role in any credible wealth preservation strategy.

What are the essential components of a generational wealth plan in Zürich, Küsnacht, Erlenbach and Zumikon?

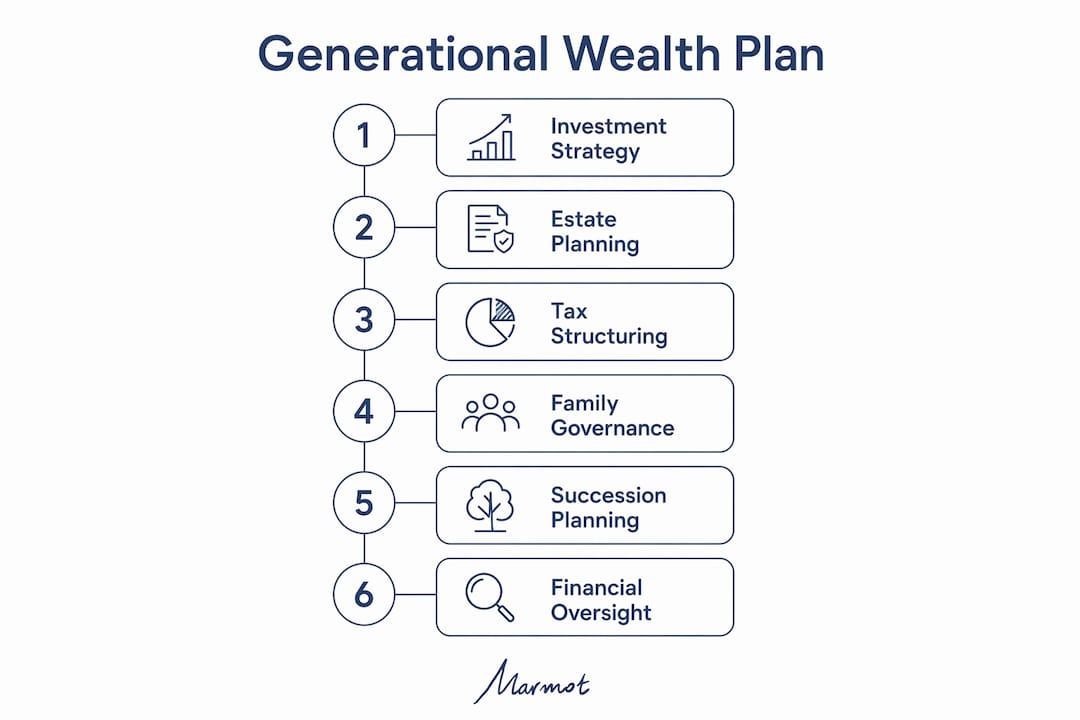

A generational wealth plan requires six coordinated components. Each one addresses a distinct risk to long-term financial security, and none works well in isolation.

Investment strategy across time horizons. A well-structured portfolio separates assets into near-term liquidity, mid-term growth, and long-term legacy buckets. This prevents families from being forced to sell long-term assets during short-term market disruptions.

Estate planning through Swiss legal instruments. Wills, inheritance contracts, and foundation structures must align with Swiss forced-heirship rules. Without this alignment, asset transfers can be challenged or reversed by law.

Tax-efficient gifting and structuring. Annual gifting rules and tax-efficient vehicles reduce the tax burden on transfers. Families who plan transfers proactively retain significantly more wealth than those who act only at death.

Family governance frameworks. A written family constitution, regular family meetings, and clear decision-making protocols prevent disputes and mismanagement. Governance failures cause more wealth loss across generations than poor investment returns.

Succession planning. Anticipating leadership transitions and asset distribution before they become urgent reduces conflict and legal costs. This applies equally to family businesses and investment portfolios.

Unified financial oversight. A single, transparent view of all assets, liabilities, and obligations allows families to make coordinated decisions. Without this, different advisers often work at cross-purposes.

Pro Tip: Start with a written family financial inventory before engaging any adviser. Knowing exactly what you own, where it is held, and how it is titled is the foundation of every other planning decision.

How do Swiss legal structures shape wealth transfer in Zumikon?

Swiss law offers specific instruments for wealth transfer, but each carries constraints that families must understand before committing to a structure.

The Familienstiftung, or family foundation, is governed by Article 335 of the Swiss Civil Code. The Swiss Federal Court interprets this provision strictly. A family foundation cannot function as a private family bank or finance ongoing living expenses. It must serve a defined family-welfare purpose, such as education, housing, or professional establishment of family members. This distinction matters enormously in practice, because families who establish foundations expecting unrestricted access to capital will find themselves constrained by law.

The Erbvertrag, or inheritance contract, is the most reliable instrument for protecting foundation endowments and managing forced heirship. Swiss forced-heirship rules cannot be bypassed simply by transferring assets into a foundation. Compulsory portions still apply to the estate, and assets transferred without a properly structured Erbvertrag remain vulnerable to clawback claims from heirs. An inheritance contract, agreed upon by all parties before death, provides legal certainty that a will alone cannot offer.

Combining wills with inheritance contracts ensures that wealth transfer aligns with forced-heirship laws while still reflecting the family’s intentions. This dual approach is standard practice for Zumikon families with complex asset structures.

A hybrid structure that combines a family foundation with a holding company or managed investment portfolio often provides the best balance of control and liquidity. The foundation holds governance authority and long-term assets, while the holding company manages operational liquidity and shorter-term investments. This hybrid approach is increasingly common among Swiss families seeking both legal protection and practical flexibility.

Pro Tip: Never establish a Familienstiftung without a concurrent Erbvertrag. The foundation protects assets during your lifetime; the inheritance contract protects the transfer at death. You need both.

For a detailed overview of estate planning essentials under Swiss law, Marmot’s dedicated guide covers the key instruments and their practical implications for affluent families.

Which investment strategies sustain wealth across generations?

Sustaining wealth across generations requires a portfolio structure that serves multiple objectives simultaneously: liquidity for current needs, growth for the next generation, and preservation for those beyond.

The bucket approach divides assets into three categories. The near-term bucket holds one to three years of living expenses in cash or short-duration bonds, protecting the family from being forced sellers during market downturns. The mid-term bucket holds diversified growth assets, including equities and real assets, with a five to fifteen year horizon. The long-term legacy bucket holds assets with the highest risk tolerance, including private equity, infrastructure, or long-duration bonds, intended for heirs rather than current income.

Tax-efficient structuring within Swiss regulations matters as much as asset selection. Holding assets through appropriate legal vehicles, timing disposals to minimise tax events, and using tax-efficient wealth structuring strategies all contribute to preserving more of what the portfolio earns. Families who ignore tax structure at the portfolio level routinely underperform those who integrate it from the outset.

Alternative investments, including private credit, real estate, and infrastructure, provide diversification beyond listed markets and generate passive income streams that are less correlated with equity volatility. These are not speculative additions. They are structural components of a portfolio designed to last decades.

Educating heirs on investment principles is as important as the portfolio itself. High-net-worth families that prioritise financial education for heirs significantly reduce the likelihood of wealth dissipation. An heir who understands compounding, diversification, and the cost of panic-selling is a far more reliable steward than one who simply inherits a portfolio they do not understand.

How does family governance influence long-term wealth security?

Family governance is the single most underestimated component of generational wealth planning. Most families focus on legal structures and investment returns, yet governance failures cause more wealth loss than market downturns or poor asset selection.

A family constitution documents shared values, decision-making processes, and expectations for each generation’s role in managing family wealth. It does not need to be a legal document. Its value lies in creating shared understanding before conflict arises, not in resolving disputes after the fact.

Regular family meetings, held at least annually, keep all members informed and engaged. These meetings should cover portfolio performance, upcoming transfers, governance decisions, and financial education for younger members. Families that meet regularly make better collective decisions and experience fewer disputes over inheritance.

Structured distributions link inheritance to milestones rather than delivering lump sums at a fixed age. Staggered or conditional distributions encourage responsibility and reduce the risk of rapid dissipation. A distribution tied to completing education, establishing a business, or reaching a savings threshold creates incentives for stewardship rather than consumption.

Financial mentoring for heirs goes beyond explaining investment basics. It involves including younger family members in real decisions, exposing them to advisers and governance meetings, and giving them supervised responsibility for a portion of the portfolio. True generational wealth combines asset growth with stewardship, and stewardship is learned through practice, not inheritance alone.

Pro Tip: Introduce heirs to the family’s advisers and governance meetings at least five years before any significant transfer. Familiarity with the people and processes reduces anxiety and improves decision-making at the moment of transition.

For families building governance frameworks alongside estate documents, this guide to legacy planning provides a practical foundation for structuring family expectations and succession intentions.

Key takeaways

Generational wealth in Zumikon requires integrating Swiss legal structures, disciplined investment, and active family governance into a single, coordinated plan.

PointDetailsIntegrated planning prevents wealth lossNearly 70% of wealthy families lose assets by the second generation without coordinated planning.Swiss legal instruments are non-negotiableAn Erbvertrag alongside a Familienstiftung provides legal protection that neither instrument offers alone.Investment structure must serve multiple generationsThe bucket approach separates liquidity, growth, and legacy assets to match different time horizons.Governance matters more than returnsFamily constitutions, regular meetings, and structured distributions prevent the governance failures that cause most wealth loss.Heir education is a planning priorityFamilies that invest in financial education for heirs significantly reduce the risk of wealth dissipation.

What I have learned from working with Zürich, Küsnacht, Erlenbach and Zumikon families on generational wealth

After working with families across Switzerland on private wealth management, the pattern I see most often is not a failure of investment strategy. It is a failure of coordination. A family has an excellent portfolio, a will drafted years ago, and a foundation set up on legal advice, but none of these components speak to each other. The estate plan does not reflect the current portfolio structure. The foundation has no governance framework. The heirs have never met the investment adviser.

The uncomfortable truth is that most wealth planning conversations happen too late. Families engage seriously only when a health event or a family dispute forces the issue. By that point, the legal options are narrower, the tax costs are higher, and the emotional stakes make rational decisions harder.

What actually works is starting the governance conversation before it feels urgent. A family that holds its first structured meeting when the eldest generation is in good health, with no immediate transfer in view, builds the habits and relationships that hold when the stakes are real. The families I have seen preserve wealth across three generations are not necessarily those with the most sophisticated legal structures. They are the ones where the second generation understood the values behind the wealth, not just the mechanics of inheriting it.

Swiss law adds a layer of complexity that families from other jurisdictions often underestimate. The Erbvertrag is not a standard instrument in most legal traditions, and the restrictions on Familienstiftung purposes surprise many clients who assumed foundations offered unrestricted flexibility. Getting local legal advice early, before structures are established, saves significant cost and complexity later.

Marmot’s approach to generational wealth planning in Zürich, Küsnacht, Erlenbach and Zumikon

Families in Zumikon who want to build lasting financial security need more than a single adviser. They need a coordinated team covering investment management, estate planning, tax structuring, and family governance, all working from the same plan.

Marmot is a FINMA-accredited wealth manager specialising in Swiss and European clients, with a particular focus on families and women navigating complex financial decisions. Marmot’s approach combines personal consultations with digital tools to give clients a clear, unified view of their financial position. Whether you are establishing a first generational plan or reviewing an existing structure, Marmot’s team provides the expert wealth management guidance needed to protect and grow what you have built. Reach out to discuss how an integrated plan can work for your family’s specific situation.

FAQ

What is long-term wealth planning in Zürich, Küsnacht, Erlenbach and Zumikon?

Long-term wealth planning in Zürich, Küsnacht, Erlenbach and Zumikon is the coordinated management of investments, estate structures, tax strategy, and family governance to preserve and transfer wealth across multiple generations within the Swiss legal framework.

Why do so many wealthy families lose their wealth by the second generation?

Nearly 70% of wealthy families lose their fortunes by the second generation, primarily because planning is fragmented and governance structures are absent, not because of poor investment performance.

What is an Erbvertrag and why does it matter in Switzerland?

An Erbvertrag is an inheritance contract agreed between parties before death. It is the most legally reliable instrument for managing forced-heirship rules and protecting assets held in Swiss family foundations from clawback claims.

Can a Swiss family foundation replace a will?

A Swiss family foundation cannot replace a will or an inheritance contract. Swiss forced-heirship rules still apply to assets transferred into a foundation, and a concurrent Erbvertrag is required to secure the transfer legally.

How does financial education for heirs protect generational wealth?

High-net-worth families that prioritise financial education for heirs significantly reduce the likelihood of wealth dissipation. Heirs who understand investment principles and governance responsibilities make better decisions at the moment of inheritance.

.webp)

.jpeg)

.svg)