Private wealth management in Switzerland is defined as a structured advisory approach that combines asset allocation, tax-efficient real estate structuring, and estate governance to preserve and transfer family wealth across generations. For high-net-worth families in Switzerland, particularly those with assets spanning Swiss stocks, private equity, and property in cantons like Graubünden, Zug, or Lucerne, getting this right is not optional. It is the difference between a legacy that lasts and one that dissolves within a generation. Firms like Marmot, KPMG, and Fidelity each contribute frameworks that shape how Swiss families approach this challenge today.

How does private wealth management in Switzerland preserve generational wealth?

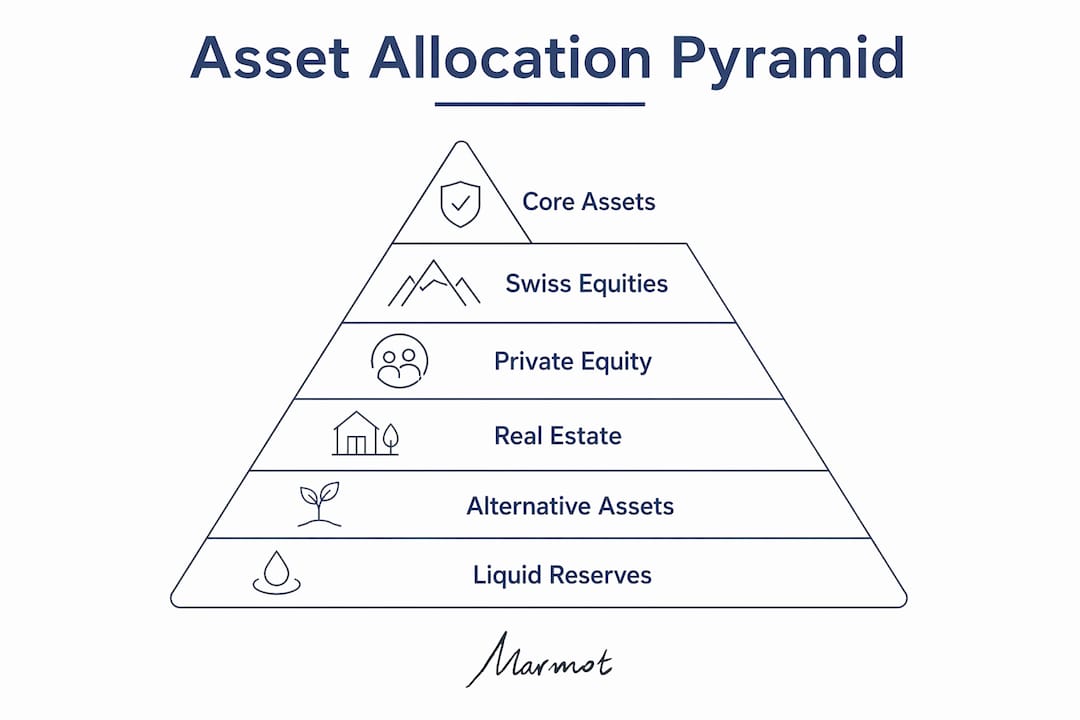

The core of any generational wealth strategy is asset allocation. Diversified Swiss stocks, private equity, and stable Swiss real estate support risk-adjusted growth that sustains wealth across generations. That combination matters because each asset class plays a different role: Swiss equities provide liquidity, private equity drives long-term growth, and real estate anchors stability.

For families based in or around, Davos, Klosters, and St Moritz, the local property market adds a tangible dimension to wealth. Swiss real estate has historically held its value well through economic cycles, making it a reliable component of a multi-generational portfolio. Private equity, meanwhile, offers access to growth that listed markets often cannot replicate, particularly in Swiss mid-market companies.

A well-structured asset mix for a high-net-worth family in Switzerland might look like this:

Swiss Equities. Blue-chip Swiss stocks such as Nestlé, Novartis, and Roche provide dividend income and long-term capital appreciation with strong governance standards.

Private Equity. Direct stakes or fund investments in Swiss and European private companies offer higher return potential over a 7–10 year horizon.

Swiss Real Estate. Residential and commercial property in Graubünden, Zug, or Zürich provides inflation protection and steady rental income.

Liquid Reserves. Cash and short-duration bonds in CHF, EUR, or USD maintain flexibility for opportunities or family needs.

Alternative Assets. Infrastructure, private debt, or commodities round out the portfolio and reduce correlation to public markets.

Balancing these classes requires ongoing review. Liquidity needs change as families grow, and tax rules shift. The goal is not to maximise returns in any single year but to maintain purchasing power and transferability across decades.

Pro Tip: Review your asset allocation at least every two years with a qualified adviser. Life events such as inheritance, divorce, or a business sale can shift your risk profile significantly, and your portfolio should reflect that.

What are the tax considerations for swiss real estate in generational planning?

Swiss real estate taxation is one of the most complex areas families must navigate. Cantonal real estate transfer taxes vary from 1% to 3.3%, and the rules differ depending on whether you are transferring rights in rem or shares in a real estate company. Several cantons, including Aargau, Glarus, Schaffhausen, Schwyz, Ticino, Uri, Zug, and Zürich, do not levy these transfer taxes at all. That distinction matters enormously when choosing where to hold property.

The abolition of imputed rental value in Switzerland has prompted many owners to consider placing property into a real estate company, often structured as an Immobilien-AG. The logic is appealing: a corporate wrapper can offer tax efficiency on an ongoing basis. But KPMG recommends modelling the tax entry ticket and future tax position carefully before making any transfer, because the upfront costs can easily outweigh the long-term benefits.

Swiss law lacks special legal entities designed specifically for real estate investment. Families typically use regulated vehicles or limited companies, each subject to a mix of federal and cantonal tax regimes. Some cantons operate a dualistic system where capital gains are taxed separately; others use a monistic approach. Looking at Davos in particular, the table below summarises key differences across cantons relevant to families in the Davos area.

| Canton | Transfer Tax | Capital Gains Tax System | Notes |

|---|---|---|---|

| Graubünden | Applies | Dualistic | Relevant for Davos and Klosters properties |

| Zug | No transfer tax | Monistic | Favourable for corporate structures |

| Lucerne | Applies | Dualistic | Clawback provision on transfers at acquisition cost |

| Zürich | No transfer tax | Monistic | Common for holding company structures |

| Schwyz | No transfer tax | Dualistic | Popular for family holding vehicles |

Lucerne deserves particular attention. Lucerne allows transfer at acquisition cost to avoid real estate capital gains tax, but this is subject to a five-year clawback provision. That means selling or restructuring within five years can trigger the very tax you sought to avoid. Families with property in multiple cantons need a coordinated plan, not a piecemeal approach.

Pro Tip: Before transferring any property into a corporate structure, commission a full tax model covering both the entry costs and the projected tax position over 10–20 years. What looks efficient today may not be in a decade.

Which estate planning tools protect wealth across generations?

Estate planning is where financial strategy meets family reality. A Fidelity survey found that 4 in 10 families worry about losing wealth quickly without proper plans in place. The risks they cite include family litigation, infighting, and unexpected tax bills. These are not abstract concerns. They are the most common reasons generational wealth erodes.

The legal tools available to Swiss families are well developed. Trusts, foundations, and family holding companies each serve different purposes. A foundation, for example, can hold assets for specific purposes such as education or philanthropy, with clear rules on distribution that reduce the scope for dispute. An irrevocable trust can ring-fence assets for a beneficiary with special circumstances, such as a child with a disability or a family member with a history of financial difficulty.

Governance matters as much as legal structure. Families that communicate their intentions clearly to heirs tend to preserve wealth more effectively than those that do not. This means having explicit conversations about values, expectations, and the conditions under which assets will be distributed. It also means documenting those conversations in a family charter or letter of wishes that sits alongside the formal legal documents.

The key estate planning tools worth considering include formal wills updated regularly to reflect Swiss succession law, family foundations for philanthropic or educational purposes, irrevocable trusts for specific beneficiary needs, shareholder agreements for family-owned businesses, and a family charter that sets out governance principles and communication expectations.

Families with assets across Davos, Verbier, Zermatt, and Zurich often find that the geographic spread of their holdings adds complexity. Each property or business interest may sit in a different canton with different rules. A coordinated estate plan, reviewed by advisers familiar with Swiss cantonal law, is the only way to manage that complexity without leaving gaps.

How do Switzerland’s TEF rules support private wealth disputes?

Private wealth disputes are more common than families like to admit. When they involve trusts, foundations, or cross-border assets, they can become protracted, expensive, and very public. Switzerland’s TEF Rules, effective 1 July 2025, offer a structured alternative to court litigation for exactly these situations.

The Supplemental Swiss Rules for Trust, Estate and Foundation Disputes are designed to handle the specific complexities that arise in private wealth conflicts. They provide a confidential arbitration framework where families can appoint experts with relevant knowledge of trust law, estate planning, or Swiss cantonal rules. That expertise is not always available in a general court setting.

Arbitration under the TEF Rules reduces the risk of protracted, public disputes and gives families with multi-jurisdictional assets greater confidence that any resolution will be enforceable. Switzerland’s reputation as a neutral, legally reliable jurisdiction makes it a natural home for this kind of mechanism. For families with assets in Davos, Zug, or Geneva, the ability to resolve a dispute privately and efficiently is genuinely valuable.

The practical implication is straightforward. If your estate plan involves a trust, foundation, or complex holding structure, consider including an arbitration clause that references the TEF Rules. This does not mean you expect a dispute. It means you are prepared for one, and that preparation protects everyone involved.

Pro Tip: Ask your estate planning lawyer to review whether your existing trust or foundation documents include an arbitration clause. If they do not, adding one now is far simpler than trying to do so in the middle of a family conflict.

Key takeaways

Preserving generational wealth in Switzerland requires combining tax-aware asset allocation, canton-specific real estate structuring, clear estate governance, and proactive dispute resolution planning.

| Point | Details |

|---|---|

| Asset allocation is the foundation | Combine Swiss equities, private equity, real estate, and liquid reserves for balanced, long-term growth. |

| Canton rules vary significantly | Transfer taxes and capital gains treatment differ across Graubünden, Zug, Lucerne, and Zurich. |

| Model tax costs before restructuring | KPMG advises calculating the full entry and exit tax position before placing property in a corporate wrapper. |

| Estate planning needs communication | Fidelity research shows 4 in 10 families risk losing wealth without clear plans and open conversations with heirs. |

| TEF Rules offer private dispute resolution | Switzerland’s new arbitration framework for trust and estate disputes, effective July 2025, protects confidentiality and enforceability. |

What i have learned about protecting family wealth in Switzerland

After working with families across Davos, Zug, and Lucerne, the pattern I see most often is not a lack of wealth. It is a lack of coordination. Families have good advisers in isolation, a tax lawyer here, a property manager there, but no one is looking at the whole picture.

The families that preserve wealth across generations tend to do three things differently. They model tax scenarios before making structural decisions, not after. They have honest conversations with their heirs about expectations, not just about assets. And they build dispute resolution into their planning from the start, rather than treating it as something that only happens to other people.

The TEF Rules are a genuinely useful development. I have seen how quickly a family dispute can become public and damaging when it ends up in court. Having a confidential, expert-led arbitration process available is a real improvement for Swiss private wealth clients.

One more thing worth saying: the abolition of imputed rental value has prompted a lot of families to rush into corporate real estate structures. Some of those decisions will look very different in ten years. The tax entry costs are real, the clawback provisions in cantons like Lucerne are real, and the long-term benefits are not guaranteed. Take your time, model it properly, and get advice from someone who understands both the federal and cantonal dimensions.

— Sophie Steinmann

How Marmot supports families in Davos with wealth preservation

If you are managing family wealth across Swiss real estate, private equity, and listed assets, the complexity can feel significant. Marmot is a FINMA-accredited wealth manager with deep expertise in wealth management in Davos, supporting families with asset allocation, tax-efficient structuring, and estate planning across CHF, EUR, and USD accounts.

Marmot’s approach combines personal advisory with clear digital tools, so you always know where your wealth stands and what the next step looks like. Whether you are reviewing your real estate structure, planning an inheritance, or simply want a second opinion on your current portfolio, Marmot offers the kind of independent wealth management that puts your family’s long-term interests first. Reach out to explore what a tailored plan could look like for you.

FAQ

What is private wealth management in Davos?

Private wealth management in Davos is a structured advisory service for high-net-worth individuals and families, covering asset allocation, tax planning, real estate structuring, and estate governance to preserve and transfer wealth across generations.

Which Swiss cantons are most favourable for real estate holding structures?

Zug, Zurich, and Schwyz do not levy real estate transfer taxes, making them more attractive for corporate holding structures. Families in Graubünden and Lucerne face transfer taxes and should model costs carefully before restructuring.

How does the TEF rules arbitration framework work?

The TEF Rules, effective 1 July 2025, provide a confidential arbitration process for trust, estate, and foundation disputes in Switzerland. Families appoint expert arbitrators and resolve conflicts privately, with outcomes that are enforceable across borders.

Why is family communication part of wealth preservation?

A Fidelity survey found that 4 in 10 families risk losing wealth quickly without proper planning. Clear communication with heirs about intentions, values, and distribution conditions significantly reduces the risk of litigation and family conflict.

Does placing Swiss property in a company always save tax?

Not necessarily. KPMG advises that transfer taxes and canton-specific capital gains rules can make corporate restructuring more expensive than expected. Lucerne’s five-year clawback provision is one example where the assumed tax saving can reverse if circumstances change.

This article is for general educational purposes only and does not constitute tax, legal, or investment advice. Tax treatment depends on individual circumstances, canton, residency, asset type, and structure. Professional advice should be sought before implementing any wealth structuring strategy.

.webp)

.jpeg)

.png)

.svg)