A tailored portfolio for women investors is a personalized investment strategy built around your specific financial goals, life circumstances, risk tolerance, and values. Generic, one-size-fits-all models consistently fail women because they ignore the structural realities that shape female financial lives: longer lifespans, career interruptions, and a strong preference for value-aligned investing. The good news is that only 53% of women feel confident managing investments today, which means the gap between where you are and where you could be is closeable with the right structure. Women who invest with personalized finance strategies built for their actual lives don’t just close that gap. They outperform.

What shapes a tailored portfolio for women investors?

Women’s financial lives follow patterns that standard portfolio models were never designed to accommodate. Understanding those patterns is the first step toward building something that actually works for you.

The most significant factor is longevity. Women in Switzerland and across the developed world live, on average, several years longer than men. That means your retirement portfolio needs to sustain income for a longer period, which shifts the entire calculus around asset allocation, withdrawal rates, and inflation protection. A portfolio built for a 20-year retirement horizon looks very different from one built for 30 years.

Career breaks add another layer of complexity. Whether for caregiving, relocation, or education, income interruptions reduce the years available for compounding and shrink pension contributions. Portfolio management for women must account for these gaps by front-loading contributions during high-earning years and building flexibility into the investment timeline.

Beyond the numbers, women prioritize long-term financial security, philanthropy, and education when designing their portfolios. This isn’t a soft preference. It’s a structural driver of portfolio construction. A woman who wants her money to support clean energy or community development needs a portfolio that reflects that, not one that defaults to whatever the market index happens to hold.

-

Longer life expectancy: Plan for 30-plus years of retirement income, not 20

-

Career breaks: Build contribution flexibility and catch-up mechanisms into your plan

-

Values-driven investing: Align holdings with sustainable investing priorities like ESG funds

-

Risk-appropriate behavior: Recognize that caution is a feature, not a flaw

Pro Tip: If you’ve taken a career break, calculate the exact contribution gap it created and set an automatic monthly transfer to close it over the next three to five years. Small, consistent amounts compound faster than you expect.

How should you structure a portfolio built for your goals?

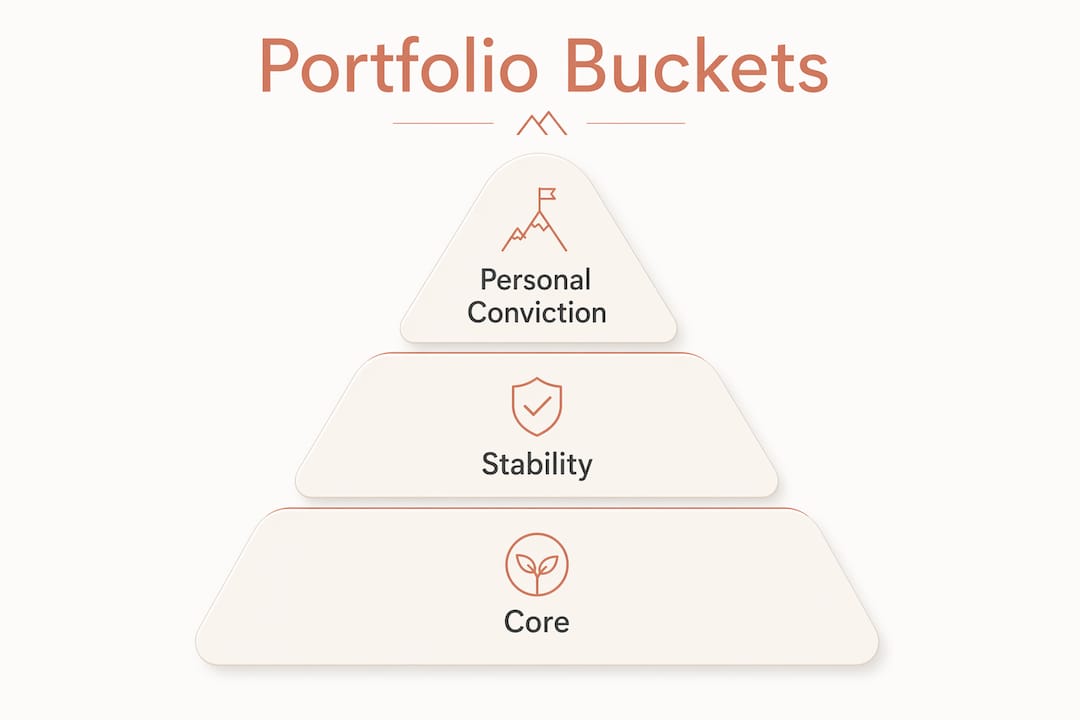

The most practical framework for investment plans for female investors is the three-bucket model. It separates your money by purpose and time horizon, which makes it far easier to stay disciplined when markets move.

Bucket one: the core. This is where 60 to 70 percent of your portfolio lives. A diversified core typically allocates 60 to 70 percent to index funds and ETFs, with the remainder in bonds or fixed income. Low-cost index funds from providers like Vanguard, iShares, or Swisscanto give you broad market exposure without the drag of high management fees. This bucket grows steadily over decades and forms the foundation of your long-term wealth.

Bucket two: stability. Bonds, fixed income instruments, and cash equivalents sit here. This bucket absorbs volatility and provides liquidity when you need it. For women with longer investment horizons, this allocation can be leaner in early years and grow as you approach retirement.

Bucket three: personal conviction. This is your 0 to 10 percent allocation to individual stocks, sector bets, or thematic funds that reflect your specific interests or beliefs. Want exposure to women-led companies, healthcare innovation, or renewable energy? This is where that goes. It keeps investing personally meaningful without putting your core wealth at risk.

One critical clarification: no evidence shows that female-specific investment products outperform standard diversified funds. The advantage comes from tailored strategy and infrastructure, not from products labeled for women. Build your portfolio around low-cost, diversified funds and customize the structure around your life, not around marketing.

| Portfolio bucket | Allocation | Purpose |

|---|---|---|

| Core index funds and ETFs | 60 to 70% | Long-term growth, low cost, broad diversification |

| Bonds and fixed income | 20 to 30% | Stability, income, volatility buffer |

| Individual stocks or themes | 0 to 10% | Personal conviction, values alignment, engagement |

Automated contributions are the infrastructure that holds this structure together. Setting a fixed monthly transfer into each bucket removes the decision fatigue that leads to inconsistent investing. Tools like VIAC, Frankly, or your bank’s standing order function make this frictionless.

Why do women’s behavioral strengths improve portfolio outcomes?

The most underappreciated edge in women-focused investment portfolios is behavioral. Research consistently shows that women outperform men by 0.4 to 1.8 percent annually, driven by patience, lower overconfidence, and consistent plan adherence. That performance gap compounds dramatically over a 30-year investment horizon.

The mechanism is straightforward. Men trade more frequently, often driven by overconfidence in their ability to time the market. Women tend to set a plan and hold it. Women employ buy-and-hold strategies that yield better returns during market volatility, precisely because they avoid the transaction costs and mistimed exits that erode male portfolios during downturns.

“Behavior is the strongest driver of investment returns. Women’s patience and discipline are their investment edge.” — WMN Magazine

The practical implication is that your portfolio structure should be designed to protect and amplify these behavioral strengths. That means building in automation so you never have to make a decision under pressure, consolidating your accounts into a single dashboard so you can see the full picture without reacting to individual positions, and setting a calendar reminder for quarterly reviews rather than checking daily.

Automating contributions and consolidating account views helps women avoid impulsive trading and improves portfolio performance. This isn’t just a convenience feature. It’s a structural advantage that turns your natural patience into a compounding machine.

Pro Tip: Set a rule for yourself: you are only allowed to rebalance your portfolio twice per year, in January and July. This single constraint eliminates most of the behavioral mistakes that cost investors money.

How do you implement and maintain your tailored portfolio?

Building a women-focused investment portfolio is a five-step process. Each step is concrete and sequenced so you can start today regardless of how much capital you have.

-

Choose a low-cost platform. In Switzerland, options include PostFinance, Swissquote, or a FINMA-accredited wealth manager like Marmot. Evaluate platforms on annual fees, fund selection, and the quality of their reporting tools. Fees above 1 percent annually will materially reduce your long-term returns.

-

Define your three buckets and target allocations. Write them down. Assign a percentage to each bucket based on your time horizon and goals. A 35-year-old with a 30-year horizon might hold 70 percent in core index funds, 20 percent in bonds, and 10 percent in thematic funds. A 55-year-old approaching retirement shifts toward 50 percent core, 40 percent bonds, and 10 percent conviction plays.

-

Set up automatic monthly contributions. Starting to invest earlier, even with small amounts, significantly increases long-term wealth compared to waiting for larger capital. A standing order of 200 Swiss francs per month started at 30 produces far more wealth by 65 than 500 francs per month started at 45.

-

Schedule semi-annual reviews. Review your portfolio in January and July. Check whether your actual allocations have drifted more than 5 percent from your targets. If they have, rebalance by selling the overweight bucket and buying the underweight one. Do not review more frequently than this.

-

Update your plan after major life changes. Marriage, divorce, a new child, a career break, or an inheritance all change your financial profile. Each of these events is a trigger to revisit your financial independence plan and adjust allocations accordingly. Your portfolio should evolve with your life, not stay frozen at the settings you chose on day one.

How do tailored portfolios build financial independence for women?

Custom investment options for women do more than generate returns. They build the confidence and control that make financial independence a real outcome rather than an abstract goal. Women’s growing financial control allows them to demand investment advice aligned with longer lifespans and values rather than one-size-fits-all models. That demand is reshaping the wealth management industry.

The confidence effect is measurable. Women who work with advisors who understand their specific circumstances report higher satisfaction with their financial plans and are more likely to stay invested during market downturns. This isn’t about hand-holding. It’s about having a plan that makes sense for your actual life, which makes it far easier to trust and follow.

Aligning your portfolio with personal values adds a motivational dimension that generic portfolios lack. When your money is invested in companies and funds that reflect what you care about, checking your portfolio stops feeling like a chore and starts feeling like progress toward something meaningful. This psychological alignment is a genuine driver of long-term investing consistency.

-

Education builds confidence: Women who understand their portfolio structure make better decisions under pressure

-

Values alignment sustains motivation: Portfolios connected to personal beliefs are easier to maintain through volatility

-

Advisory support closes structural gaps: Personalized financial advice for women addresses income variability and longevity in ways generic models cannot

-

Early action compounds: Every year you delay costs more than any single investment decision you will ever make

Key takeaways

A tailored portfolio for women investors outperforms generic models because it addresses the specific behavioral strengths, life circumstances, and values that drive long-term wealth creation.

| Point | Details |

|---|---|

| Customize for your life stage | Adjust allocations for career breaks, longevity, and evolving goals rather than using a generic model. |

| Use the three-bucket structure | Split holdings into core index funds, bonds, and a small conviction allocation for values-aligned investing. |

| Protect your behavioral edge | Automate contributions and limit reviews to twice yearly to preserve your natural patience and discipline. |

| Start early with any amount | Small monthly contributions started early outperform larger contributions started late due to compounding. |

| Tailoring is about infrastructure | The advantage comes from personalized strategy and automation, not from female-labeled investment products. |

What I’ve learned from listening to women investors

After years of working with women at different stages of their financial lives, the single most consistent finding surprises most people: the biggest barrier isn’t knowledge. It’s the feeling that the standard financial system wasn’t built with you in mind. That feeling is correct. Most portfolio models were designed around male career trajectories, male risk profiles, and male retirement timelines. When you try to fit your life into that model, it doesn’t work, and you blame yourself for the misfit.

What I’ve seen change outcomes is the moment a woman sees a portfolio structure that actually reflects her life. Not a product marketed to women, but a genuine plan that accounts for her career break, her longer retirement horizon, her preference for sustainable funds, and her goal of funding her children’s education before her own retirement. That moment of recognition transforms skepticism into commitment. And committed investors outperform.

The pitfall I see most often is waiting. Waiting for more money, more knowledge, more certainty. The research is unambiguous: starting earlier with less beats starting later with more. The women I’ve watched build genuine financial independence didn’t start with large portfolios. They started with a structure that fit their life and the discipline to keep contributing through every market cycle.

— Tom

How Marmot supports women investors with personalized portfolios

Marmot is Switzerland’s only FINMA-accredited wealth manager built exclusively for women and families. Over 350 women have already transformed their financial situations through Marmot’s hybrid approach, which combines personal consultations with digital tools to build portfolios that reflect your actual goals, values, and timeline. Whether you’re based in Basel, Geneva, or Davos, Marmot’s advisors specialize in the kind of personalized finance for women that generic wealth managers simply don’t offer. From the Money Makeover Quiz to ongoing financial coaching, every service is designed to build your confidence alongside your wealth. Explore Marmot’s wealth management for women to see what a portfolio built for your life actually looks like.

FAQ

What is a tailored portfolio for women investors?

A tailored portfolio for women investors is a personalized investment strategy designed around your specific financial goals, life circumstances, risk tolerance, and values. It differs from generic models by addressing factors like longer life expectancy, career breaks, and values-driven investing preferences.

Do women-specific investment products outperform standard funds?

No. Research shows that female-specific products do not outperform standard diversified funds. The performance advantage comes from personalized strategy, automated infrastructure, and behavioral discipline, not from products labeled for women.

How often should women review their investment portfolios?

Semi-annual reviews, in January and July, are sufficient for most investors. More frequent reviews increase the risk of reactive, emotion-driven decisions that reduce long-term returns.

Why do women tend to outperform men as investors?

Women outperform men by 0.4 to 1.8 percent annually due to lower overconfidence, less frequent trading, and stronger plan adherence. These behavioral traits reduce transaction costs and prevent the mistimed exits that erode returns during market volatility.

How much money do I need to start a tailored investment portfolio?

You don’t need a large sum to start. Portfolio growth simulations confirm that starting with small amounts early produces significantly more wealth than waiting to accumulate larger capital, thanks to the compounding effect over time.

.webp)

.jpeg)

.svg)