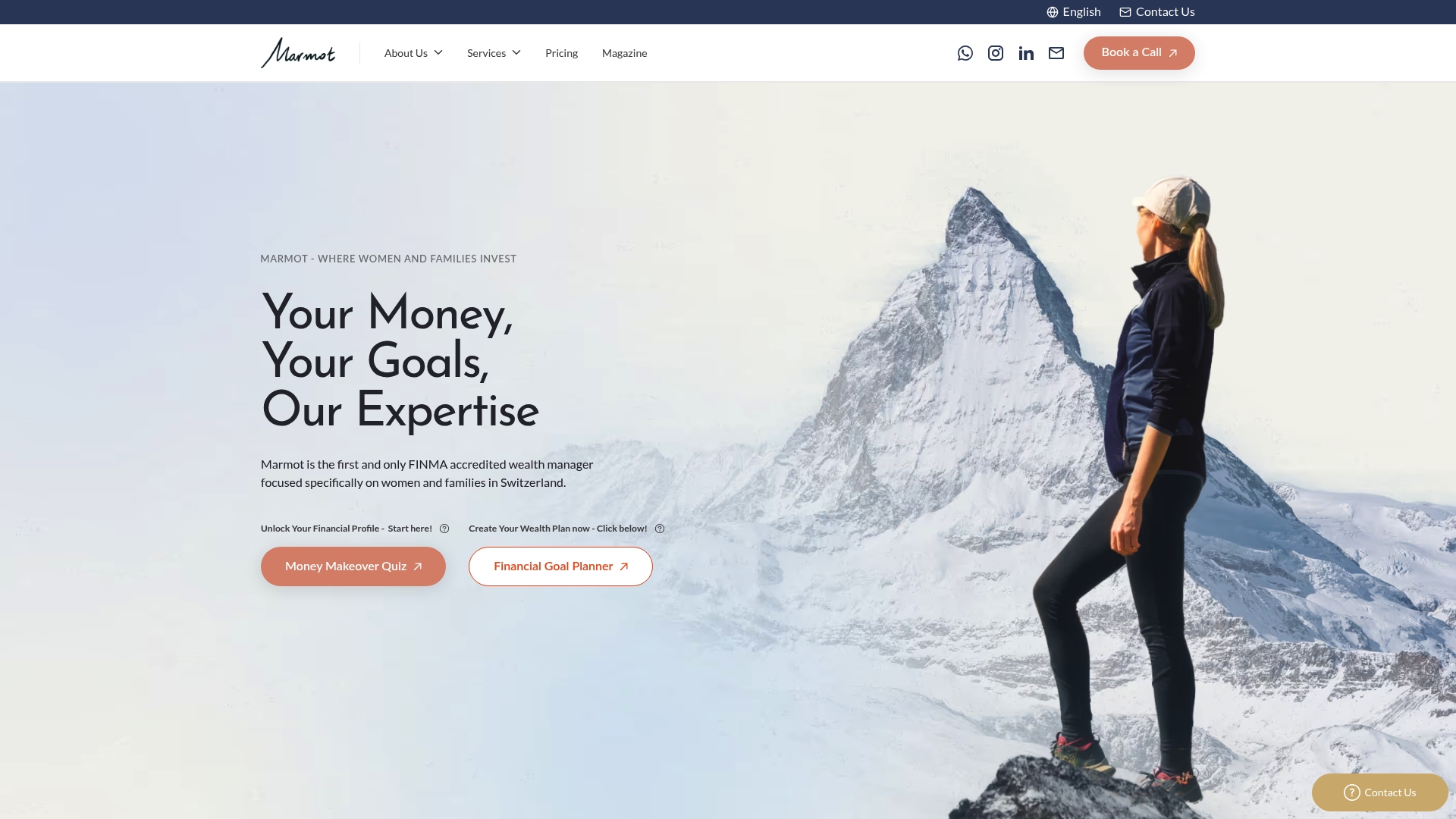

Women principals are defined not merely as asset holders but as economic architects who shape financial outcomes across generations, households, and organisations. Women-controlled wealth grew 51% globally between 2018 and 2023, outpacing total financial wealth growth of 43%. That is a remarkable shift, and it carries real weight for women leading schools and businesses in Switzerland. Yet the role of women principals in wealth is not simply about accumulating more. It is about managing, directing, and stewarding wealth with clarity and purpose across complex life stages. Many affluent women still face what researchers call a financial fluency gap, and closing it requires strategies built specifically for how women lead and live.

How women principals’ wealth management differs from traditional models

Traditional wealth management was designed around a single earner with a linear career and one retirement horizon. That model does not fit most women principals today, and it certainly does not fit those managing organisations in, for example, Zürich, Basel, or Zug while also navigating family responsibilities and career transitions.

Advisory models are evolving towards a stewardship framework that accounts for multi-stakeholder responsibility. This means thinking beyond your own retirement to consider the financial wellbeing of family members, employees, and sometimes entire communities. Women principals in education, for example, often influence institutional budgets, staff welfare, and long-term school strategy simultaneously. That is a form of wealth stewardship, even when it is not labelled as such.

Longer lifespans also change the equation. Women in Switzerland live, on average, several years longer than men, which means retirement savings must stretch further and investment strategies must remain flexible well into later decades. Career breaks for caregiving, which remain more common among women, create gaps in pension contributions that compound over time if not addressed deliberately.

Intergenerational governance frameworks that formalise tax preferences, succession planning, and beneficiary design give women principals a structured way to manage these complexities. Rather than reacting to financial events as they arise, this approach builds a clear ruleset that holds across leadership transitions and life changes.

Pro Tip: Ask your wealth adviser to map your financial responsibilities across three horizons: your own retirement, any dependants you support, and any organisational or legacy goals you hold. If they cannot do this, find an adviser who can.

What is the financial fluency gap for women principals?

Financial fluency is not the same as financial literacy. Literacy means understanding concepts. Fluency means knowing what to do and when, particularly under pressure or during major life transitions. An HSBC and Ipsos survey in 2026 found that only a minority of affluent women feel prepared for the complex financial decisions ahead of them, despite being poised to control unprecedented levels of wealth. That gap between wealth and confidence is the core problem.

For women principals, the fluency gap often surfaces at specific moments: a promotion, a divorce, an inheritance, a school leadership transition, or a health change. These are exactly the moments when financial decisions carry the most consequence, and they are also the moments when most people feel least prepared.

Scheduling financial decision checkpoints tied to life and career events is one of the most practical ways to close this gap. Rather than reviewing your finances on a fixed annual calendar, you build a trigger-based system. A new role triggers a pension review. A relationship change triggers a beneficiary update. A significant market movement triggers a portfolio rebalance conversation.

Another common barrier is the lack of tailored advice. Generic financial guidance rarely accounts for the wave-like progression of women’s careers, where income rises, pauses, and rises again in patterns that differ from the steady linear climb traditional models assume. Seeking out advisers who understand this pattern, and who can work with resources like financial advice for women, makes a measurable difference in outcomes.

Pro Tip: Create a personal financial calendar with four annual checkpoints linked to your career and life events, not just the tax year. Review your pension, investments, and insurance at each one.

Asset allocation strategies for women principals in Switzerland

Switzerland offers a specific and genuinely attractive set of investment options for women principals managing portfolios in CHF, EUR, or USD. The Swiss market rewards patience, diversification, and local knowledge, which aligns well with the stewardship approach most women principals naturally favour.

Swiss stocks, private equity, and real estate are the three core asset classes worth understanding in depth. Swiss equities, particularly in sectors like pharmaceuticals, financial services, and precision engineering, offer stability and dividend income that suits long-term wealth goals. Companies listed on the SIX Swiss Exchange have historically demonstrated resilience during global downturns, which matters when your wealth serves multiple stakeholders.

Real estate in Swiss financial centres such as Zürich, Basel, Lausanne, and Zug has delivered consistent long-term returns, though entry costs are high and liquidity is lower than equities. For women principals with a longer investment horizon, direct property or real estate funds can serve as a meaningful inflation hedge. Locations like Küsnacht, Zollikon, and Meilen on Lake Zürich, or Meggen near Lucerne, attract both domestic and international buyers, which supports price stability.

Private equity deserves attention as a diversification tool, particularly for principals with higher risk tolerance and a five-to-ten year investment horizon. Swiss private equity access has broadened in recent years, and selective exposure can meaningfully improve portfolio returns beyond what public markets offer.

The table below summarises how these three asset classes compare across the dimensions most relevant to women principals in Switzerland.

| Asset class | Liquidity | Return potential | Suitable horizon | Key consideration |

|---|---|---|---|---|

| Swiss equities | High | Moderate to high | 3 to 10 years | Dividend income and market stability |

| Swiss real estate | Low | Moderate | 7 to 15 years | Inflation hedge, high entry cost |

| Private equity | Very low | High | 5 to 10 years | Requires higher minimum investment |

Pension fund planning sits alongside these asset classes as a non-negotiable priority. Switzerland’s three-pillar pension system, covering state pension, occupational pension, and private savings, offers significant tax advantages when used deliberately. Voluntary contributions to Pillar 3a, for example, reduce taxable income and build retirement capital simultaneously. Women principals who have experienced career breaks should model the pension gap this creates and consider catch-up contributions where possible.

International tax considerations also apply if you hold assets or income across borders. Switzerland’s double taxation agreements with most European countries and the United States create planning opportunities, but they require specialist advice to use correctly. Marmot works exclusively with CHF, EUR, and USD accounts, which covers the currency exposure most Swiss-based women principals face.

How does female leadership affect wealth outcomes?

The impact of female leaders on wealth extends well beyond personal finance. Female CEOs lead firms with roughly 95% higher CSR scores than their male counterparts. That is not a marginal difference. It reflects a fundamentally different approach to what organisations are for and how success is measured.

For women principals in education and business, this translates into a values-led approach to financial stewardship. Responsible investment, philanthropy, and ethical governance are not add-ons. They are central to how female principals define and protect wealth over time. This approach also tends to produce more resilient organisations, because it builds trust with stakeholders rather than optimising purely for short-term returns.

“Women are not just accumulating wealth but redefining financial success through management, allocation, and legacy considerations that focus on resilience and family continuity.” — State Street Global Advisors

Gender-balanced leadership improves financial outcomes by up to 25%, according to research from McKinsey and BCG. This finding holds across industries and geographies, including Switzerland. Organisations led or co-led by women demonstrate stronger risk management and greater adaptability during periods of uncertainty. For women principals managing institutional or personal wealth, this is both an affirmation and a practical argument for seeking out advisers and governance structures that reflect the same values.

The connection between women’s leadership roles and sustainable financial outcomes is increasingly well-documented. Principals who understand this connection can use it to make a stronger case for the investment strategies and governance frameworks they choose to adopt.

Key takeaways

Women principals who treat wealth as stewardship rather than accumulation consistently achieve stronger, more resilient financial outcomes across generations.

| Point | Details |

|---|---|

| Stewardship over accumulation | Women principals manage wealth for multiple stakeholders, not just personal retirement. |

| Financial fluency gap | Knowing when to act matters as much as knowing what to do; build trigger-based decision checkpoints. |

| Swiss asset allocation | Diversify across Swiss equities, real estate, and private equity with pension planning at the centre. |

| Female leadership and CSR | Female-led organisations show up to 95% higher CSR scores, linking values to long-term financial resilience. |

| Tailored advice is non-negotiable | Generic financial models do not account for women’s career patterns; seek advisers who do. |

Why the stewardship model changed how I think about this

I used to assume that the main challenge for women principals managing wealth was access. Access to information, access to good advisers, access to the right products. And access does matter. But after working with women across Switzerland, from school principals in Lucerne to business leaders in Zug and Davos, I have come to believe the deeper issue is framing.

Most financial conversations still start with “how much do you want to retire with?” That is the wrong question for most women principals. The right question is “what are you responsible for, and over what time horizon?” When you reframe wealth management as stewardship rather than accumulation, the entire strategy changes. You start thinking about governance, about beneficiary design, about the values you want your portfolio to reflect.

The Swiss market is genuinely well-suited to this approach. The stability of Swiss institutions, the quality of local advisers in cities like Basel and Zürich, and the structure of the three-pillar pension system all support long-term, multi-stakeholder thinking. But you have to ask for it explicitly. Most advisers will default to a standard model unless you push for something more tailored.

The women I have seen make the most progress are not necessarily the ones with the most assets. They are the ones who got clear on what they were actually managing wealth for, and then built a strategy around that clarity. That is the shift worth making.

— Sophie Steinmann

Wealth management built for women principals in Switzerland

Marmot is the only FINMA-accredited wealth manager in Switzerland built exclusively for women and families. Whether you are based in Zürich, Basel, Geneva, Davos, or anywhere across the country, Marmot offers personalised wealth management that accounts for your career stage, your responsibilities, and your values. Over 350 women have already worked with Marmot to take control of their financial futures, using a combination of personal coaching and digital tools designed to make complex decisions feel manageable. If you are ready to move from reactive to deliberate in how you manage your wealth, Marmot is a practical next step. You can also explore wealth management in Basel or Geneva if you want locally grounded advice.

FAQ

What is the role of women principals in wealth management?

Women principals act as stewards of wealth rather than simple asset accumulators, managing financial outcomes across multiple stakeholders and generations. This stewardship role requires flexible, life-stage aligned strategies that go beyond standard retirement planning.

How can women principals close the financial fluency gap?

Scheduling financial decision checkpoints tied to career and life events, such as promotions, relationship changes, or health shifts, is the most effective method. Pairing this with an adviser who understands women’s non-linear career patterns significantly improves decision confidence.

What asset classes suit women principals investing in Switzerland?

Swiss equities, real estate in centres like Zürich, Basel, and Lausanne, and selective private equity form the core of a well-diversified portfolio. Pension fund planning through Switzerland’s three-pillar system adds a tax-efficient foundation to any allocation strategy.

How does female leadership influence financial outcomes?

Female-led organisations show up to 95% higher CSR scores and benefit from up to 25% better financial performance linked to gender-balanced leadership. These outcomes reflect a values-driven approach to governance that supports long-term wealth resilience.

Do women principals need a specialist wealth adviser?

Generic advisory models are built around linear careers and single retirement horizons, which rarely match women principals’ actual financial lives. A specialist adviser who understands intergenerational stewardship, Swiss pension structures, and career-break planning delivers meaningfully better outcomes.

.webp)

.jpeg)

.png)

.svg)