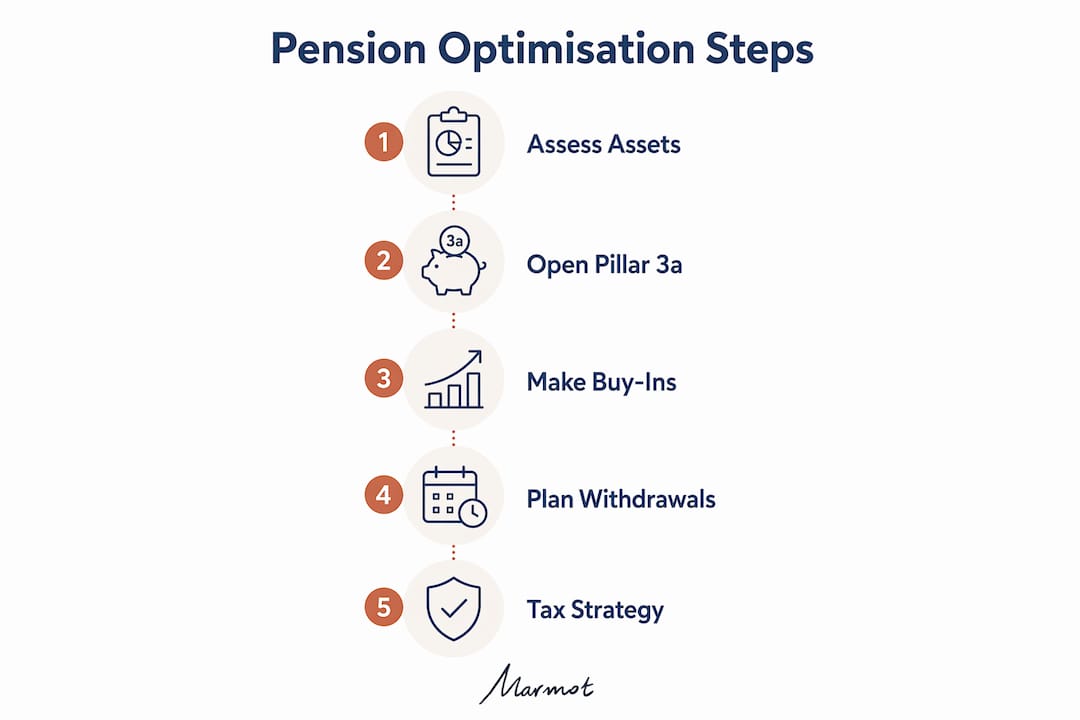

Swiss pension optimisation in Lausanne is the active management of your contributions and withdrawals across the three-pillar system to maximise retirement income and reduce your tax bill. For Swiss citizens and expatriates living in Lausanne, this matters more than most people realise. Vaud canton applies progressive tax rates that can significantly erode pension capital if you withdraw without a plan. The good news is that the Swiss system, built on Pillar 1 (AHV), Pillar 2 (occupational pension), and Pillar 3a (private savings), offers real room to act. The key is knowing when and how to move. Marmot works with clients in Lausanne to do exactly that.

How does the Swiss three-pillar system work and what are the optimisation opportunities?

The Swiss pension system rests on three pillars, each serving a distinct purpose. Understanding how they interact is the foundation of any serious retirement plan.

Pillar 1 (AHV) is the state social security layer. It provides a basic income floor in retirement, funded by mandatory contributions throughout your working life. You cannot contribute extra to AHV, but you can protect your entitlement by avoiding gaps in your contribution record, which matters especially for expatriates who arrive in Switzerland mid-career.

Pillar 2 is your occupational pension, managed through your employer’s pension fund. Contributions are mandatory above a certain income threshold, but you can also make voluntary top-up payments, known as buy-ins or rachats. These buy-ins are fully tax deductible and can boost retirement capital significantly when timed well in the final decade of your career.

Pillar 3a is your private pension account. It is voluntary, tax-deductible, and the most flexible tool available to you. In 2026, employees can contribute up to CHF 7,258 annually, while self-employed individuals can contribute up to CHF 36,288. That gap reflects the fact that the self-employed have no Pillar 2, so the state allows a larger private provision.

The optimal planning window is between ages 45 and 50, with detailed plans finalised 10–15 years before retirement. Starting earlier gives you more room to restructure accounts, make buy-ins, and time withdrawals without rushing.

What strategies optimise Pillar 3a contributions and withdrawals for tax efficiency?

Pillar 3a is where most people in Lausanne leave money on the table. The contribution itself is straightforward, but the real gain comes from how you structure and eventually withdraw your accounts.

The single most effective move is opening multiple Pillar 3a accounts rather than one. Swiss law allows you to hold several accounts simultaneously. When you retire, you withdraw them in separate years, which means each withdrawal is taxed independently at a lower rate. Staggered withdrawals from multiple accounts reduce the tax rate compared to a single lump sum, saving thousands of Swiss francs in progressive cantons like Vaud.

The risk of getting this wrong is real. Combining capital withdrawals from Pillar 3a and Pillar 2 in the same year triggers taxation on the combined total. Withdrawing CHF 100,000 from a 3a account and CHF 200,000 from your pension fund together means the tax authority calculates the rate on CHF 300,000. Spreading those withdrawals across different years cuts that combined figure and the rate that applies to it.

In Vaud, the tax savings from annual Pillar 3a contributions are also substantial. Contributing CHF 7,258 to Pillar 3a on a CHF 100,000 income can save approximately CHF 2,200 to CHF 2,500 in taxes each year. That is a direct, immediate return on your contribution before any investment growth.

Pro Tip: Open your first additional Pillar 3a account as early as possible, even if you only contribute a small amount. The number of accounts you can withdraw from separately in retirement is fixed by how many you opened during your working years. You cannot split an existing account retroactively.

When choosing a provider for your Pillar 3a, look beyond the interest rate. Providers like Viac, Finpension, and Frankly offer investment-linked accounts that historically outperform savings accounts over a 10-year horizon. The choice of provider affects your long-term balance, not just your annual tax deduction.

| Scenario | Annual tax saving (Vaud, CHF 100k income) |

|---|---|

| Max employee contribution CHF 7,258 | CHF 2,200–2,500 |

| No Pillar 3a contribution | CHF 0 |

| Self-employed max contribution CHF 36,288 | Significantly higher (marginal rate applies) |

How to optimise Pillar 2 buy-ins and withdrawal choices to maximise benefits?

Pillar 2 buy-ins are one of the most tax-efficient tools available to higher earners in Lausanne. A voluntary buy-in fills a gap in your pension fund contribution history, and the full amount is deductible from your taxable income in the year you make it.

The practical impact is significant. If you are in a high marginal tax bracket in Vaud, a CHF 50,000 buy-in could reduce your tax bill by CHF 15,000 or more in that year alone. The capital then grows within the pension fund and increases your retirement benefit. The one constraint is that buy-ins must remain invested for at least three years before you can withdraw the capital. Planning the timing matters.

When you reach retirement, you face a choice between taking your Pillar 2 as a monthly annuity or as a lump sum. The annuity gives you a guaranteed income for life. The lump sum gives you flexibility but requires you to manage the capital yourself. Many people in Lausanne choose a partial lump sum, taking enough capital to cover specific goals while keeping a portion as annuity income.

Pro Tip: If both you and your spouse have Pillar 2 benefits, stagger your withdrawals across different tax years. Each withdrawal is taxed separately, so splitting them reduces the combined tax burden considerably.

Coordinating your Pillar 2 withdrawal with your Pillar 3a withdrawals is equally important. Taking both in the same year pushes your total taxable capital into a higher bracket. A five-year withdrawal plan, starting with Pillar 3a accounts and finishing with Pillar 2, is a common and effective approach for Lausanne residents.

What are the long-term pension implications of early retirement in Lausanne?

Early retirement is appealing, but the financial cost is often underestimated. Retiring before 65 in Switzerland reduces your AHV pension permanently. Pension cuts of around 6.8% per year of early retirement reduce your monthly income, and those cuts compound over a 30-year retirement span.

Retiring at 60 instead of 65 can mean a monthly income reduction of CHF 600 to CHF 1,000. Over 30 years, that adds up to a very large shortfall. The maths rarely favours early retirement unless you have substantial private assets or a well-funded Pillar 2 with voluntary buy-ins to compensate.

The conversion rate applied to your Pillar 2 capital also falls if you retire early. Pension funds use a conversion rate to calculate your annuity from your accumulated capital. The earlier you retire, the lower that rate, because the fund expects to pay you for longer.

“The most common mistake I see is people planning early retirement without modelling the income gap over 25 to 30 years. The numbers look manageable at 60 but become uncomfortable at 75 when savings are depleted.”

A gap analysis is the right starting point. This means calculating your projected AHV entitlement, your Pillar 2 benefit at your target retirement age, and your Pillar 3a balance, then comparing the total against your expected living costs. If there is a gap, late-career buy-ins into Pillar 2 are the most tax-efficient way to close it. You can find more detail on structuring your private savings in Marmot’s guide to Pillar 3a planning.

How does Vaud canton tax policy affect your pension withdrawal strategy?

Vaud applies a progressive capital withdrawal tax to Pillar 2 and Pillar 3a withdrawals. The rate rises as the total capital withdrawn in a given year increases. This is the central reason why withdrawal timing and sequencing matter so much for pension planning in Lausanne.

Cantonal tax differences are often overlooked, but they can account for thousands of francs in savings when you sequence withdrawals intelligently. Vaud sits in the higher range of cantonal tax rates, which makes the case for staggering withdrawals across multiple years particularly strong.

Some clients consider moving to a lower-tax canton before retirement. This is a legitimate strategy, but it requires planning at least five years in advance. Swiss tax law applies the cantonal rate of your place of residence at the time of withdrawal, so a move to a canton like Schwyz or Zug before you start drawing down can reduce your withdrawal tax materially.

| Withdrawal approach | Tax outcome in Vaud |

|---|---|

| Single year: CHF 300,000 combined (Pillar 2 + 3a) | High progressive rate on full amount |

| Staggered: CHF 100,000 per year over 3 years | Lower rate applied to each tranche separately |

| Spouse coordination: withdrawals in different years | Further reduction through independent assessments |

Pro Tip: Start your withdrawal planning at least five years before your target retirement date. In Vaud, the difference between a well-timed and a poorly timed withdrawal strategy can easily exceed CHF 20,000 in total tax paid.

Key takeaways

Effective Swiss pension optimisation in Lausanne requires coordinating contributions, buy-ins, and withdrawals across all three pillars with Vaud’s progressive tax rates in mind.

| Point | Details |

|---|---|

| Open multiple Pillar 3a accounts | Withdraw each account in a separate year to reduce progressive tax in Vaud. |

| Max out annual Pillar 3a contributions | Contributing CHF 7,258 as an employee saves CHF 2,200–2,500 in Vaud taxes each year. |

| Use Pillar 2 buy-ins strategically | Voluntary buy-ins are fully tax deductible and must stay invested for at least three years. |

| Never combine large withdrawals in one year | Taking Pillar 2 and Pillar 3a capital together triggers higher combined tax rates. |

| Start planning between ages 45 and 50 | This window gives you time for buy-ins, account restructuring, and withdrawal sequencing. |

Why I think most people in Lausanne are planning their pensions too late

Most people I speak with start thinking seriously about their pension at 58 or 59. By that point, the best opportunities have already passed. The multi-account Pillar 3a strategy only works if you opened those accounts years earlier. Buy-ins into Pillar 2 need three years to become withdrawable. And withdrawal sequencing across five years requires you to start before you actually need the money.

The other thing I see constantly is people ignoring Vaud’s cantonal tax rates until it is too late to act. They focus on the national rules and miss the local detail that makes the biggest practical difference. A client who moves from Lausanne to a lower-tax canton two years before retirement and staggers their Pillar 3a withdrawals over four years can save a meaningful amount compared to someone who does nothing. That is not a complex strategy. It just requires starting early enough.

My honest view is that pension planning in Switzerland rewards people who treat it like a project with a timeline, not a form to fill in when they turn 64. If you are between 45 and 55 and living in Lausanne, now is the right time to sit down and map it out properly. The system is genuinely generous if you use it well.

— Sophie Steinmann

How Marmot supports pension planning in Lausanne

Marmot is a FINMA-accredited wealth manager working with Swiss residents and expatriates in Lausanne to build retirement plans that actually reflect local tax rules and personal goals. If you are unsure whether your current Pillar 3a structure is set up for tax-efficient withdrawals, or you want to understand whether a Pillar 2 buy-in makes sense for your situation, Marmot can help you work through it clearly. The team combines personal consultations with digital tools to give you a plan you can act on. Reach out to Marmot’s team for personalised pension advice tailored to your situation in Lausanne.

FAQ

What is the Pillar 3a contribution limit in Switzerland for 2026?

Employees can contribute up to CHF 7,258 to Pillar 3a in 2026. Self-employed individuals without a Pillar 2 can contribute up to CHF 36,288.

How many Pillar 3a accounts can I open in Switzerland?

Swiss law does not cap the number of Pillar 3a accounts you can hold. Opening several accounts early allows you to withdraw them in separate years and reduce your tax burden in progressive cantons like Vaud.

Are Pillar 2 buy-ins tax deductible in Switzerland?

Yes. Voluntary buy-ins into your Pillar 2 pension fund are fully deductible from your taxable income in the year you make them. The capital must remain invested for at least three years before withdrawal.

What happens to my pension if I retire early in Switzerland?

Retiring before 65 reduces your AHV pension by approximately 6.8% for each year of early retirement. Monthly income can fall by CHF 600 to CHF 1,000 for those retiring at 60, with the shortfall compounding over a 30-year retirement.

Does it matter which canton I live in when I withdraw my pension?

Yes. Vaud applies higher progressive capital withdrawal taxes than lower-tax cantons such as Schwyz or Zug. Moving canton before retirement and staggering withdrawals across years are both legitimate strategies to reduce the total tax paid on pension capital.

.webp)

.jpeg)

.png)

.svg)