Stocks are defined as ownership shares in a company, granting the holder a claim on profits and, in most cases, voting rights in corporate decisions. Bonds, by contrast, are debt instruments: the investor lends money to an issuer, whether a government or corporation, and receives fixed interest payments, known as coupon payments, before the principal is returned at maturity. Understanding the bonds vs stocks difference is not merely academic. It determines how much risk you carry, how your portfolio behaves in a downturn, and whether your money grows or simply holds its ground. Swiss market data stretching back to 1900, compiled by Pictet, shows that these two asset classes behave in fundamentally different ways over time, making the choice between them one of the most consequential decisions any investor faces.

What is the difference between bonds and stocks?

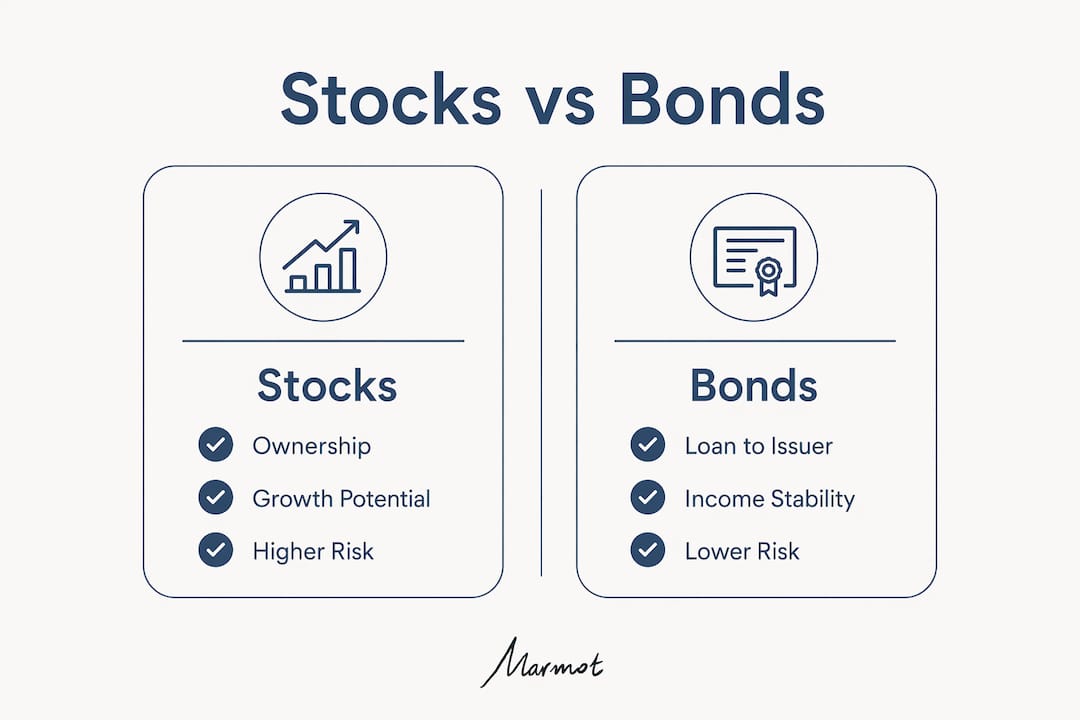

Stocks represent a share of ownership in a company. When you buy shares in a Swiss firm listed on the Swiss Performance Index, you become a part-owner, entitled to a portion of its profits through dividends and to vote on major corporate decisions. Your return depends on how well the company performs and how the market values it at any given moment.

Bonds work on an entirely different principle. You lend money to an issuer, such as the Swiss Confederation or a large corporation, and in return you receive regular coupon payments at a fixed rate. At the end of the bond’s term, the issuer repays the original sum. Bonds do not provide voting rights; they are a creditor relationship, not an ownership one.

The core contrast is this: stocks offer growth potential and ownership, while bonds offer income and relative stability. Both have a place in a well-constructed portfolio, but they serve different purposes and carry different risks. Knowing which to favour, and in what proportion, is the foundation of sound investment planning.

How do bonds work and what are their main features?

A bond has three defining components: the issuer, the coupon, and the maturity date. The issuer borrows capital from investors and commits to paying a fixed coupon, typically expressed as a percentage of the bond’s face value, at regular intervals. On the maturity date, the issuer repays the face value in full.

Bonds are traded on exchanges, which means their market price fluctuates before maturity. When interest rates rise, existing bond prices fall, because newer bonds offer higher coupons. When rates fall, existing bond prices rise. This interest rate sensitivity is one of the most misunderstood features of bond investing.

Not all bonds carry the same risk. The main categories include:

-

Government bonds: Issued by sovereign states, such as Swiss Confederation bonds. These carry the lowest default risk.

-

Corporate bonds: Issued by companies. Risk varies widely depending on the issuer’s financial health.

-

Senior bonds: Rank first in the creditor queue if the issuer goes bankrupt, offering greater protection.

-

Subordinated bonds: Rank behind other creditors in a bankruptcy. They carry a higher risk of total loss and compensate investors with higher coupon rates.

-

Convertible bonds: Can be converted into shares of the issuing company under certain conditions, blending debt and equity characteristics.

Bonds play a specific role in a portfolio: they reduce overall volatility and provide a predictable income stream. For investors who need capital preservation alongside some return, they are a core building block.

Pro Tip: When comparing bonds, always check whether they are senior or subordinated. The coupon rate alone does not tell you the full risk story. A higher coupon often signals higher default risk, not a better deal.

What are stocks and how do they differ in ownership and risk?

Stocks grant the investor a genuine stake in a business. That ownership comes with two potential sources of return: dividend income, paid from company profits, and capital gains, realised when the share price rises above the purchase price. Stocks offer dividend income and capital gains potential but come with greater price fluctuations linked to company profitability and market sentiment.

The key characteristics of stocks include:

-

Ownership and voting rights: Shareholders vote on board appointments, mergers, and other major decisions.

-

Dividend income: Companies may distribute a portion of profits to shareholders, though dividends are never guaranteed.

-

Capital gains: If the company grows and the market recognises that growth, the share price rises.

-

Higher volatility: Share prices react to earnings reports, economic data, geopolitical events, and investor sentiment, often sharply.

-

Long-term growth potential: Over decades, equities have consistently outperformed bonds in nominal terms.

Swiss stocks have historically exhibited much higher volatility than bonds, with annualised standard deviations of 19% versus 5.2% respectively since 1900. That figure is striking. It means that in any given year, a Swiss equity portfolio could swing dramatically in either direction, while a bond portfolio stays comparatively calm.

The trade-off is clear. Stocks carry more short-term risk, but they also deliver more long-term reward. For investors with a long time horizon and the temperament to hold through downturns, equities are the primary engine of wealth creation.

How do returns and risks of stocks and bonds compare historically in Switzerland?

The Swiss market provides one of the longest and most reliable datasets in the world for comparing these two asset classes. The numbers are unambiguous.

Swiss stocks achieved an annual nominal return of 6.8%, considerably higher than the 3.9% return for Swiss bonds from 1900 to 2025. In real terms, after adjusting for inflation, stocks returned approximately 4.6% per year versus 1.8% for bonds. That gap compounds significantly over decades.

| Asset class | Nominal annual return | Real annual return | Annualised volatility |

|---|---|---|---|

| Swiss stocks | 6.8% | 4.6% | 19.0% |

| Swiss bonds | 3.9% | 1.8% | 5.2% |

| 60/40 portfolio | 6.0% | approx. 3.5% | 12.0% |

The 60/40 portfolio, comprising 60% Swiss stocks and 40% Swiss bonds, achieved a 6% annualised return with volatility of 12%. That is a meaningful reduction in risk for a relatively modest sacrifice in return.

Bonds also serve as a buffer during market crises. In 29 out of 37 years where Swiss stocks were negative, Swiss bonds showed positive returns, cushioning losses. That pattern is not coincidental. It reflects the fact that stocks and bonds react differently to economic changes: stocks are driven by earnings and growth expectations, while bonds respond to interest rates and demand for safety.

“No diversified Swiss portfolio held for any 10-year period since 1912 has produced a loss. That record speaks directly to the power of combining stocks and bonds across a full market cycle.”

This historical record does not guarantee future results, but it does illustrate a principle that has held across two world wars, multiple recessions, and several currency crises. Diversification between stocks and bonds has consistently protected Swiss investors from catastrophic permanent loss.

What practical considerations should investors keep in mind?

Choosing between stocks and bonds is not a binary decision. Most investors benefit from holding both, with the proportion determined by their individual circumstances. The following factors shape that decision.

-

Time horizon: Investors with 20 or more years before they need their capital can afford to hold a higher proportion of equities. Short-term investors, or those approaching retirement, typically shift towards bonds to protect accumulated wealth.

-

Risk tolerance: Volatility is not just a number. It translates into real portfolio swings that can unsettle even experienced investors. If a 20% drop in portfolio value would prompt you to sell, a heavy equity allocation is not appropriate for you.

-

Income needs: Bonds provide predictable coupon income. Investors who need regular cash flow from their portfolio, such as retirees, often rely on bonds to meet living expenses without selling assets.

-

Interest rate environment: Rising interest rates reduce the market value of existing bonds. In a rising-rate environment, shorter-duration bonds or inflation-linked bonds may be preferable to long-dated fixed-rate instruments.

-

Portfolio diversification: Modern portfolio theory emphasises combining stocks and bonds to balance growth and stability. Bonds often rise when stocks fall, which is precisely why a blended portfolio reduces overall risk without proportionally reducing return.

For investors interested in global funds management strategies, the same principle applies internationally: diversification across asset classes remains the most reliable method of managing risk across market cycles.

Pro Tip: Do not assume bonds are always “safe.” In a rising interest rate environment, long-duration bonds can lose significant market value. Match bond duration to your investment horizon.

A common misconception is that bonds are boring or irrelevant for growth-oriented investors. The data from Switzerland’s asset classes for women investors shows that even growth-focused portfolios benefit from a bond allocation, particularly during periods of equity market stress.

Key takeaways

Stocks deliver higher long-term returns than bonds, but a blended portfolio of both reduces volatility significantly without sacrificing proportionate gains, as Swiss market data from 1900 to 2025 confirms.

| Point | Details |

|---|---|

| Stocks vs bonds defined | Stocks represent ownership; bonds represent a loan to an issuer paying fixed interest. |

| Return difference | Swiss stocks returned 6.8% annually versus 3.9% for bonds from 1900 to 2025. |

| Volatility contrast | Swiss stocks showed 19% annualised volatility versus 5.2% for bonds over the same period. |

| Diversification benefit | A 60/40 Swiss portfolio achieved 6% returns with only 12% volatility, reducing risk materially. |

| Bond types matter | Subordinated bonds carry higher default risk than senior bonds, reflected in higher coupon rates. |

My perspective on balancing bonds and stocks in Switzerland

Working with clients across Switzerland and Europe, I have noticed a consistent pattern: investors tend to underestimate bonds until they experience their first serious equity downturn. Then they overestimate them. Neither extreme serves a portfolio well.

The Swiss market is unusual in global terms. Its equity market is heavily concentrated in a small number of very large, internationally active companies. That concentration means Swiss equities can behave differently from broader European or global indices, and it makes bond diversification even more valuable here than in more diversified markets.

What I find most instructive is the 29-out-of-37 figure. In nearly 80% of the years when Swiss stocks fell, bonds rose. That is not luck. It is the structural difference between an ownership claim and a creditor claim, playing out across decades of market history. Understanding that relationship is what separates investors who stay the course from those who panic and sell at the worst possible moment.

The practical implication for international clients based in Switzerland is straightforward: your allocation between stocks and bonds should reflect your time horizon and income needs, not your mood about the market. Reviewing that allocation with a qualified adviser, at least annually, is not optional. It is the work.

— Sophie Steinmann

How Marmot can support your investment planning

Marmot is a FINMA-accredited wealth manager focused exclusively on clients in Switzerland and Europe, managing portfolios in CHF, EUR, and USD. The team works with women, families, and international clients who want a clear, structured approach to portfolio construction, including the right balance between equities and fixed income.

Whether you are building a portfolio from scratch or reviewing an existing allocation, Marmot provides personalised guidance grounded in Swiss market expertise. The portfolio diversification strategies Marmot applies are informed by the same long-term data that underpins this article. For clients who want direct access to that expertise, contact Marmot’s advisers to discuss your specific financial situation and goals.

FAQ

What is the main difference between a bond and a stock?

A stock represents ownership in a company, while a bond is a loan to an issuer that pays fixed interest and returns the principal at maturity. Stocks carry higher growth potential; bonds offer more predictable income and lower volatility.

Are bonds safer than stocks for Swiss investors?

Bonds have historically shown far lower volatility than Swiss stocks, with annualised standard deviations of 5.2% versus 19% since 1900. However, bonds carry their own risks, including interest rate risk and, for subordinated bonds, elevated default risk.

What is a good stocks-to-bonds ratio for a balanced portfolio?

A 60/40 split between Swiss stocks and bonds has historically delivered around 6% annualised returns with 12% volatility, making it a widely referenced starting point. The right ratio depends on your time horizon, income needs, and risk tolerance.

Do bonds lose value when interest rates rise?

Yes. When interest rates rise, the market price of existing bonds falls, because newer bonds offer higher coupon rates. Investors holding bonds to maturity still receive the full face value, but those who sell before maturity may realise a loss.

Can I hold both stocks and bonds in a Swiss investment account?

Yes. Most Swiss investment accounts and wealth management mandates allow you to hold a combination of equities and fixed income instruments. Marmot’s wealth management in Zurich service includes portfolio construction across both asset classes for international clients.

.webp)

.jpeg)

.svg)