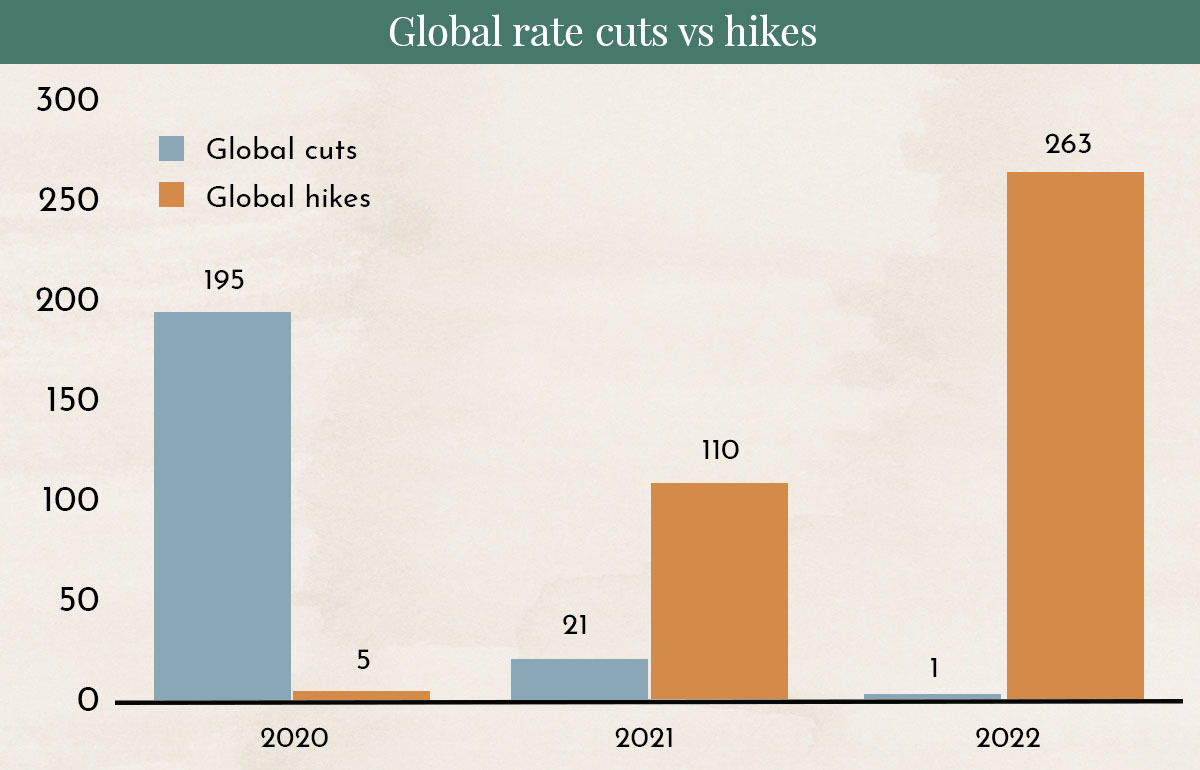

Chart of the Week

In 2020, most central banks were still cutting interest rates, but the tide has clearly turned. Central banks around the world are now raising interest rates.

Why this matters

Central banks strongly influence financial markets through their policies. Their actions usually have the greatest impact on asset prices. When central banks sharply cut interest rates, as they did in 2020, it is generally very positive for both stock and bond investors and supports rising prices.

However, policy has now shifted. Rising interest rates mean falling prices for bond investors. Over the past 30 years, investors could be fairly confident that if they bought a bond and had to sell it before maturity, they would likely realize a small or larger capital gain. From now on, however, it is clear that if you buy a bond and need to sell it before maturity, you are more likely to incur a capital loss. Anyone buying bonds now should be prepared to hold them until maturity.

Stock prices also behave differently in this kind of market environment. Volatility increases significantly. Announcements by central banks regularly push markets sharply lower — most recently last Friday in the United States. US Federal Reserve Chair Jerome Powell said in an interview that interest rates now need to rise faster than previously expected. Following this statement, stock markets fell by nearly 3%. Strong corporate earnings are then needed to continue driving prices higher.

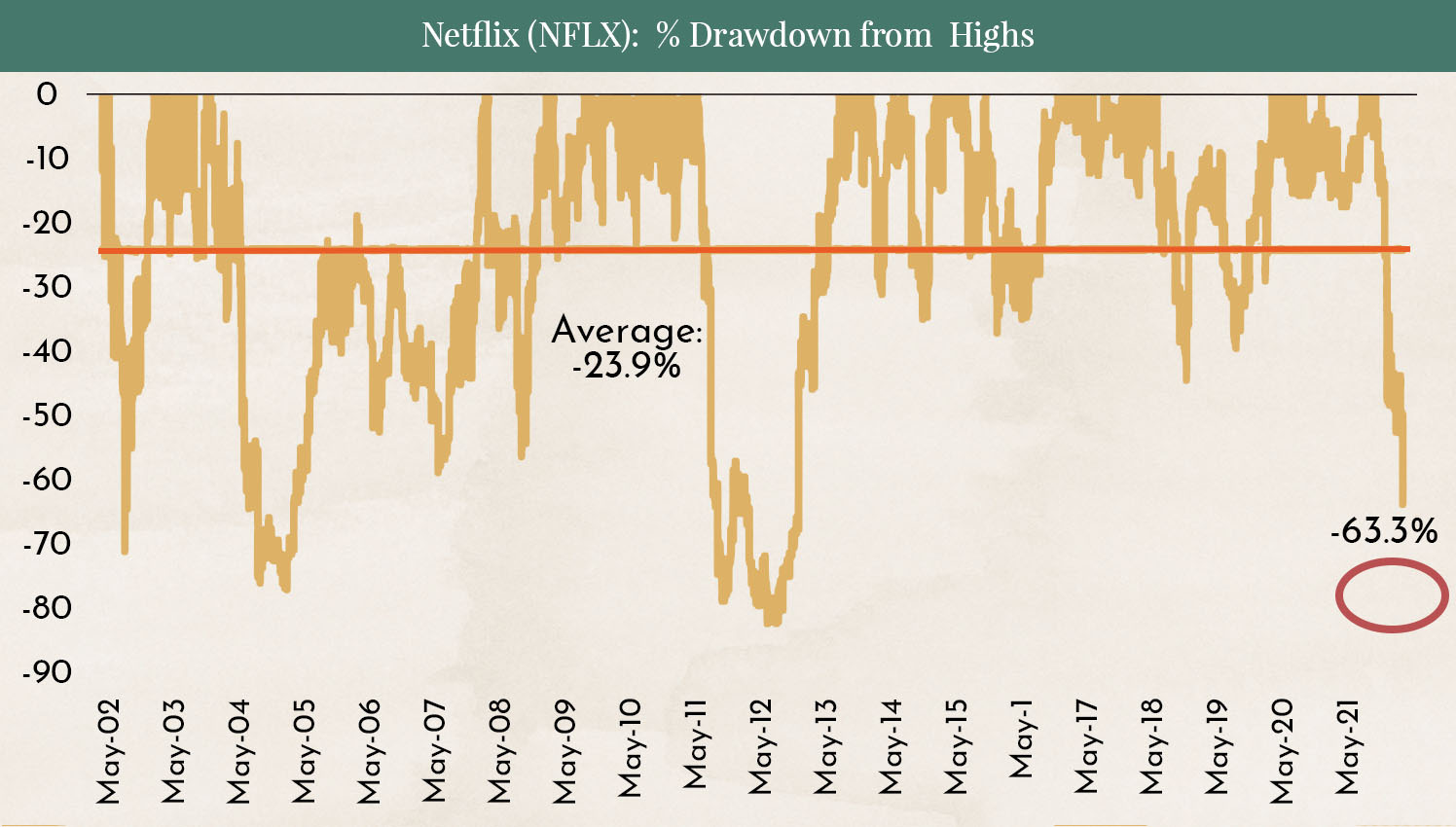

Netflix: A Predictable Stock Price Crash

On Thursday, Netflix announced declining subscriber numbers. The stock plunged by nearly 30% in a single day. Such a sharp drop may seem difficult to understand. In reality, it should have been clear to everyone that after the exceptional growth during the COVID period, people would start going out again and spend less time watching TV. Most investors were also already aware that many users share their passwords with friends. In addition, consumers have clearly noticed the growing number of competing streaming services, such as Amazon Prime Video and Disney+. Sometimes, it helps to apply common sense when buying stocks.

The chart shows the maximum losses investors could have suffered with Netflix stock since its IPO in 2002. Since its peak last November, the stock has lost more than 60% of its value. For bargain hunters, it is starting to look interesting, but it may still be too early to buy. Prices could potentially fall even further, with declines of 75% to 85% still possible.

There is also a well-known stock market saying that applies here: “Never catch a falling knife.” You should not try to catch a falling knife mid-air. It is far safer to wait until it hits the ground — only then can you pick it up without getting hurt.

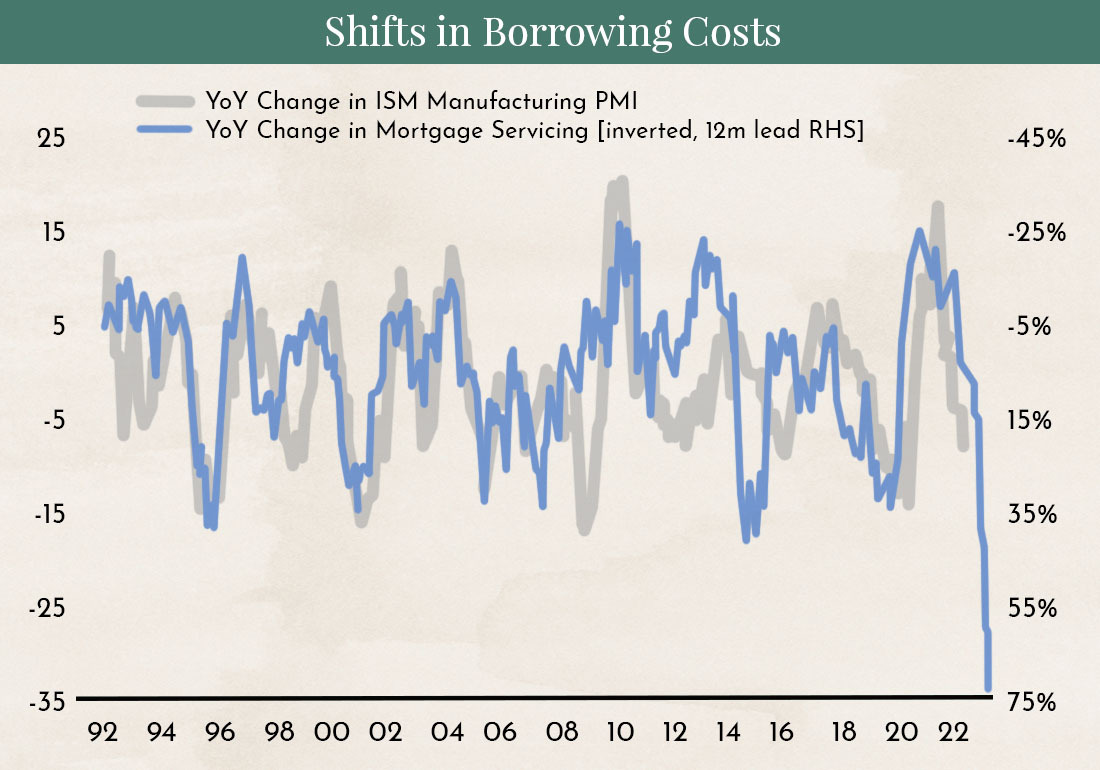

High Interest Rates Are Slowing Growth

For Americans and their sense of well-being, two things are especially important: their car and their home. More than 60% of Americans own a home. Gasoline prices have nearly doubled over the past year, and used car prices have surged over the last six months. Now, homeowners are also being hit.

The chart shows the interest rate for a 30-year mortgage in the United States. Since 1984, rates had steadily declined. However, the trend already reversed in 2021. While this may not look dramatic in historical terms on the chart, mortgage rates have nearly doubled.

The chart compares the rising costs for homeowners with the ISM Index. The Purchasing Managers’ Index (PMI), also known as the ISM Manufacturing Index or ISM Purchasing Managers’ Index, is the most important and reliable leading indicator of economic activity in the United States. It is published by the Institute for Supply Management, a U.S.-based nonprofit organization headquartered in Tempe.

The chart shows the relationship between these two indicators. When financing costs for homes rise, consumers have less money available to spend on goods and services. The doubling of financing costs means additional monthly expenses of around USD 1,000 for the average American homeowner — or as much as USD 12,000 per year.

Rising financing costs are the most effective way for central banks to cool down an overheating economy.

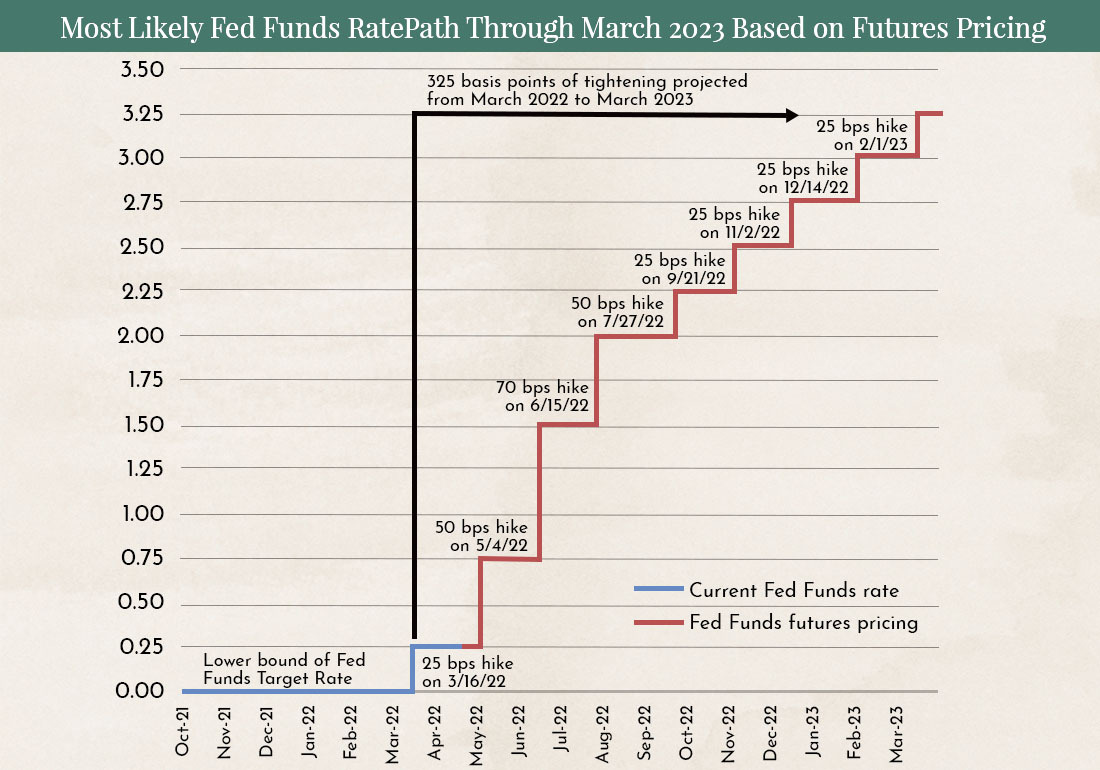

Although interest rates have already risen sharply, experts expect much more to come:

The chart shows the 0.25% interest rate hike already implemented in March 2022 (blue) and the future rate hikes expected from the U.S. Federal Reserve (Fed), based on futures market pricing (red).

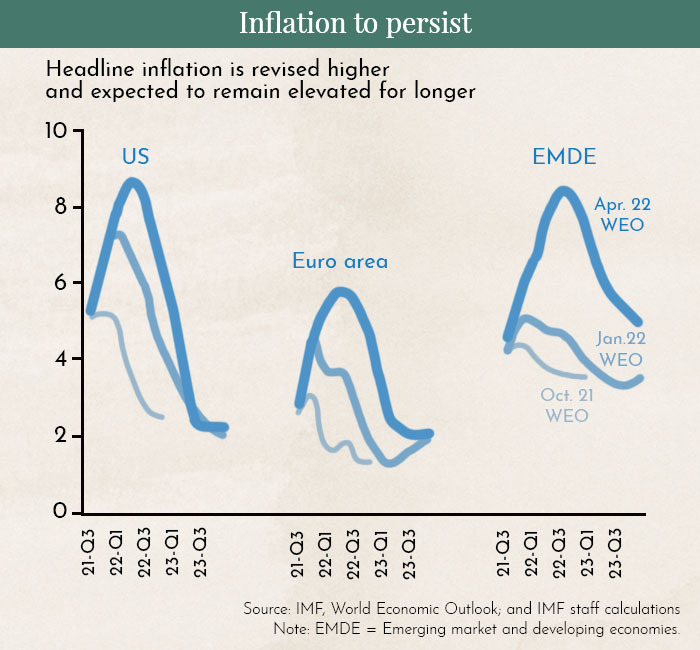

In our view, too much attention is being placed on the nominal inflation figure:

The chart shows how significantly experts — including the International Monetary Fund — misjudged the situation. The light blue line represents the IMF’s expectations from October 2021, when inflation was expected to peak in the third quarter of 2021. Now, the peak is expected to occur one year later (dark blue line).

We fear that the U.S. Federal Reserve may be overcorrecting significantly and slowing the economy too aggressively. The consequence could be a recession.

Normally, inflation is driven by strong demand. In such cases, it makes sense for central banks to curb demand, as shown above, by increasing costs — for example, through higher financing costs for homeowners.

At present, however, we are seeing high inflation because supply chains are still disrupted due to COVID, and energy prices are rising sharply as a result of the war in Ukraine. In other words, we are currently facing problems on the supply side rather than the demand side. In such a situation, slowing down demand does not make much sense.

Disclaimer:

The content in these blogs is intended solely for general informational purposes and to help potential clients gain an understanding of how we work. It does not constitute recommendations to buy or sell assets and should not be considered investment advice. Marmot.Finance cannot assess whether or how the statements made align with your investment objectives or risk profile. If you make investment decisions based on this blog post, you do so entirely at your own risk and responsibility. Marmot.Finance cannot be held liable for any losses you may incur as a result of the information contained in this blog post. The products mentioned are not recommendations but are intended to illustrate how Marmot.Finance works and selects such products. Marmot.Finance is completely independent and does not earn compensation from product providers in any form.

.webp)

.jpeg)

.jpeg)

.svg)