Winners and Losers of the Ukraine Crisis, Investor Sentiment at Its Lowest Level Since 2007

Chart of the Week

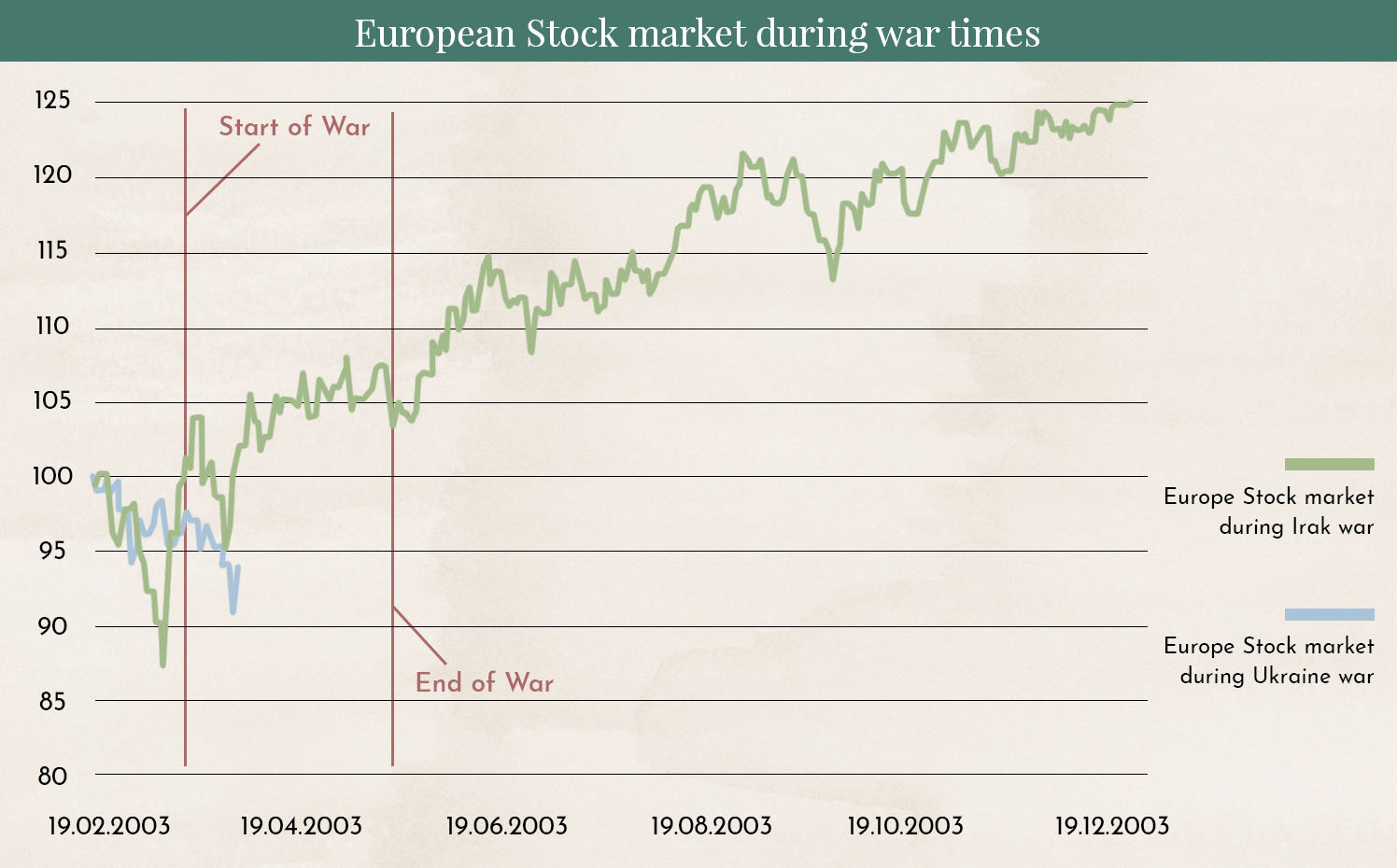

Why This Matters

The 2003 Iraq War shows many parallels to the current situation in our view. A world power attacks a sovereign state in an attempt to replace its government, while the world watches helplessly. Back then, the global supply of oil and gas was also a major concern. The aggressor first gains control of the airspace and then advances toward the capital from multiple directions. The Gulf War began on March 20, 2003, and ended on May 1, 2003. We believe this is roughly the timeframe that can also be expected for the war in Ukraine.

The European stock market reacted differently in 2003 than many expected. Once the initial shock of the outbreak of war had passed, the market stabilized and began to rise again. The same could happen in 2022. A well-known stock market saying goes: “Buy when the cannons thunder.”

Is Putin’s Strategy Working?

What completely surprised many observers was not only the outbreak of the war, but especially Putin’s justification for it. In the lead-up to the war, Putin’s focus had been on sending a signal that NATO should not expand further eastward. However, in the explanations Putin later gave on television for the attack on Ukraine, he effectively questioned the legitimacy of all states that became independent after the collapse of the USSR. This represents a massive (verbal) escalation and will lead to a complete reassessment of the security situation in Europe. Furthermore, with the attack on Ukraine, Russia has violated countless agreements it had signed since 2014.

In the first week of the war, it appeared that Putin’s strategy would fully succeed. Europe and the United States were divided over sanctions, and the agreed upon measures were largely insufficient. Over the weekend, however, the decision was made to exclude Russia from the international payment system SWIFT. This is the first measure that could severely impact both Russia and its general population. However, with China’s support, Russia is also likely to withstand this.

The only sanction that would truly be effective would be to stop purchasing raw materials from Russia immediately. However, this would require a broad and coordinated plan. Within approximately two weeks, the energy reserves of European countries would be depleted. More oil would need to come from the Gulf region, and the United States would have to support Europe with emergency energy supplies. Even then, the European population would need to be prepared for the rationing of oil and gas. Entire industries would have to halt operations due to shortages of steel and aluminum. Especially now, as companies are recovering from the COVID crisis, this could be the final blow for many. Are Europe and the United States prepared for such an approach? We doubt it and therefore unfortunately expect that Putin will ultimately prevail and that his strategy will succeed.

Winners and Losers of the Ukraine Crisis

Losers of the Ukraine Crisis:

- Europe: A completely new risk assessment for future investments in the former USSR states will now take place. Investment activity is expected to decline significantly, particularly in all non-NATO countries.

- Ukraine: The entire population, and especially all companies with factories and production facilities in Ukraine, will be affected. Due to embargoes, no business is likely to be conducted with Ukraine following a Russian occupation. A significantly higher level of unemployment is to be expected.

Winners of the Crisis:

- Companies operating in the weapons and/or security sector: This is likely to lead to a massive militarization of NATO and Europe in general. Over many years, security infrastructure has been significantly reduced.

- Commodities: Gold gained 5% following the outbreak of the war but has now returned to the same level as at the start of the conflict. However, having a small gold position in a portfolio may still be beneficial if the situation continues to escalate. Oil prices have risen by more than 50% since last November. We believe a consolidation is more likely at this point. We expect the same for wheat, where prices have increased by 45% since last November.

- Energy Transition: Many countries are planning to become carbon neutral by 2030 or 2040. In addition to environmental arguments, there are now also security-related reasons supporting this transition. This is likely to accelerate projects that have previously been politically blocked. The faster the energy transition is completed, the sooner Europe will become less dependent on energy supplies from Russia. Stocks of companies in the alternative energy sector delivered very strong returns in 2020 but consolidated in 2021. This consolidation may now be over.

- We assume that central banks, particularly the U.S. Federal Reserve, will reduce the number of interest rate hikes this year or refrain from implementing the increase planned for March. This is likely to support stock markets in general.

Investor Sentiment at Its Lowest Level Since 2007.

The chart shows a survey by the American Association of Individual Investors (AAII). The number of bears (investors expecting declining prices) was only higher in 2013 than it is today.

The chart shows how stock market returns have performed since 1987 when the proportion of investors expecting negative market performance was this high. Historically, there has been a 97% probability that prices would be higher six months later than they were at the time.

Disclaimer:

The content in these blogs is intended solely for general information purposes and to help potential clients gain an understanding of how we work. They do not constitute recommendations to buy or sell assets and should not be considered investment advice. Marmot.Finance cannot assess whether or how the statements made align with your investment objectives and risk profile. If you make investment decisions based on this blog post, you do so entirely at your own risk and responsibility. Marmot.Finance cannot be held liable for any losses that may arise from the information contained in this blog post. The products mentioned are not recommendations but are intended to demonstrate how Marmot.Finance works and selects such products. Furthermore, Marmot.Finance is completely independent and does not earn any compensation from product providers in any form.

.webp)

.jpeg)

.jpeg)

.svg)