Chart of the Week

Last Friday was a Triple Witching Day on the stock market. This term refers to a financial market event that takes place on the third Friday of certain months. During Triple Witching, three types of financial derivative contracts — stock options, stock index futures, and stock index options — all expire on the same day.

Why This Matters

On these days, traders and investors must make decisions regarding their options and futures positions, which can lead to potential market shifts (and opportunities). This may result in increased trading activity and heightened price volatility. In such an environment, opportunities can emerge. However, due to the risks associated with Triple Witching, it is crucial for market participants to remain disciplined and maintain strict risk management.

As the chart above shows, on such days derivative transactions with a volume of more than $2 trillion sometimes need to be settled. To ensure this process runs smoothly, major banks and trading firms aim to keep volatility as low as possible. If options that have been worthless for weeks suddenly gain value, a dangerous dynamic involving margin calls and substantial losses can trigger daily market swings of 5–10%.

The Triple Witching dates for 2024 are:

- March 15, 2024.

- June 21, 2024.

- September 20, 2024. Fed.

- December 20, 2024. Fed.

The September and December dates stand out in particular. In the same week, on Wednesday, decisions by the U.S. Federal Reserve regarding interest rate cuts are expected. Currently, markets anticipate the first rate cut in September and the third cut of the new cycle in December. If central banks negatively surprise investors, these two weeks could carry significant crash potential. Inexperienced investors in derivatives trading may be better off staying away from the market during these periods to avoid losing all their gains.

New Energy Sources – The Difficulty of Investing in Trends

The energy transition is on everyone’s mind. Billions are expected to be invested over the coming years in the production and storage of new, more sustainable energy sources.

Alongside the shift toward sustainable energy, energy demand continues to rise due to population growth and the emergence of millions of people in Asia and emerging markets into the new middle class. Depending on optimistic or pessimistic estimates, global energy demand is expected to increase by between 30% and 70% by 2050.

The expected global increase in energy demand by 2050 depends heavily on various factors, such as population growth, economic expansion, and technological advancements in energy efficiency and production.

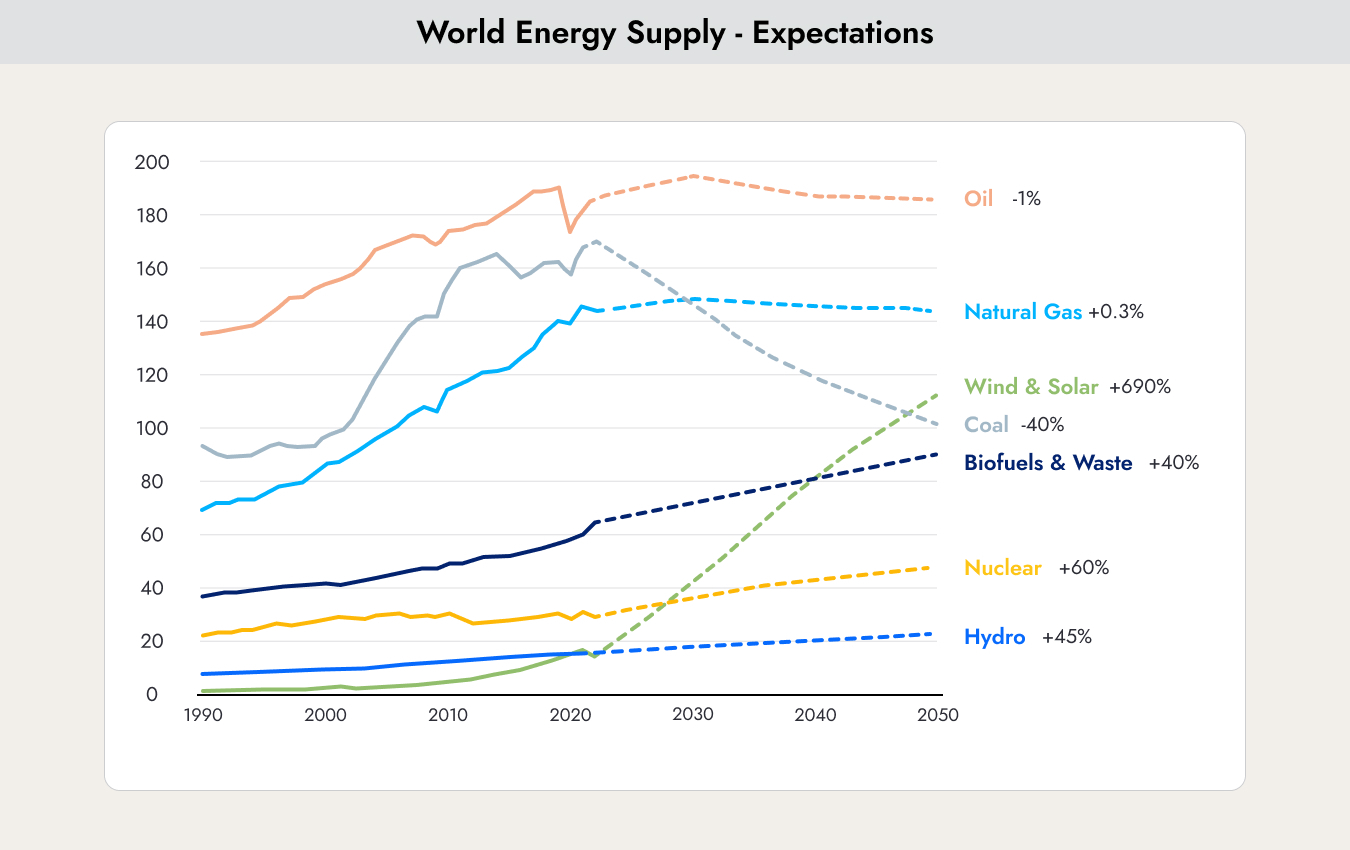

The chart illustrates the projected development of various energy sources through 2050. It clearly shows that wind and solar energy have the greatest growth potential, with a projected increase of 690%. Nuclear energy (+60%) and hydropower (+45%) are also expected to expand. In contrast, coal usage is projected to decline by 40%, while oil demand is expected to decrease slightly by 1%. Natural gas, meanwhile, is forecast to see only marginal growth of 0.3%.

How can investors benefit from this trend? At first glance, the answer seems simple. Investing in the “new energy” theme should generate strong returns. A projected increase of 690% would appear to benefit companies in this sector as well as investors.

Given these opportunities, many new energy ETFs were launched. But has investing in them actually paid off?

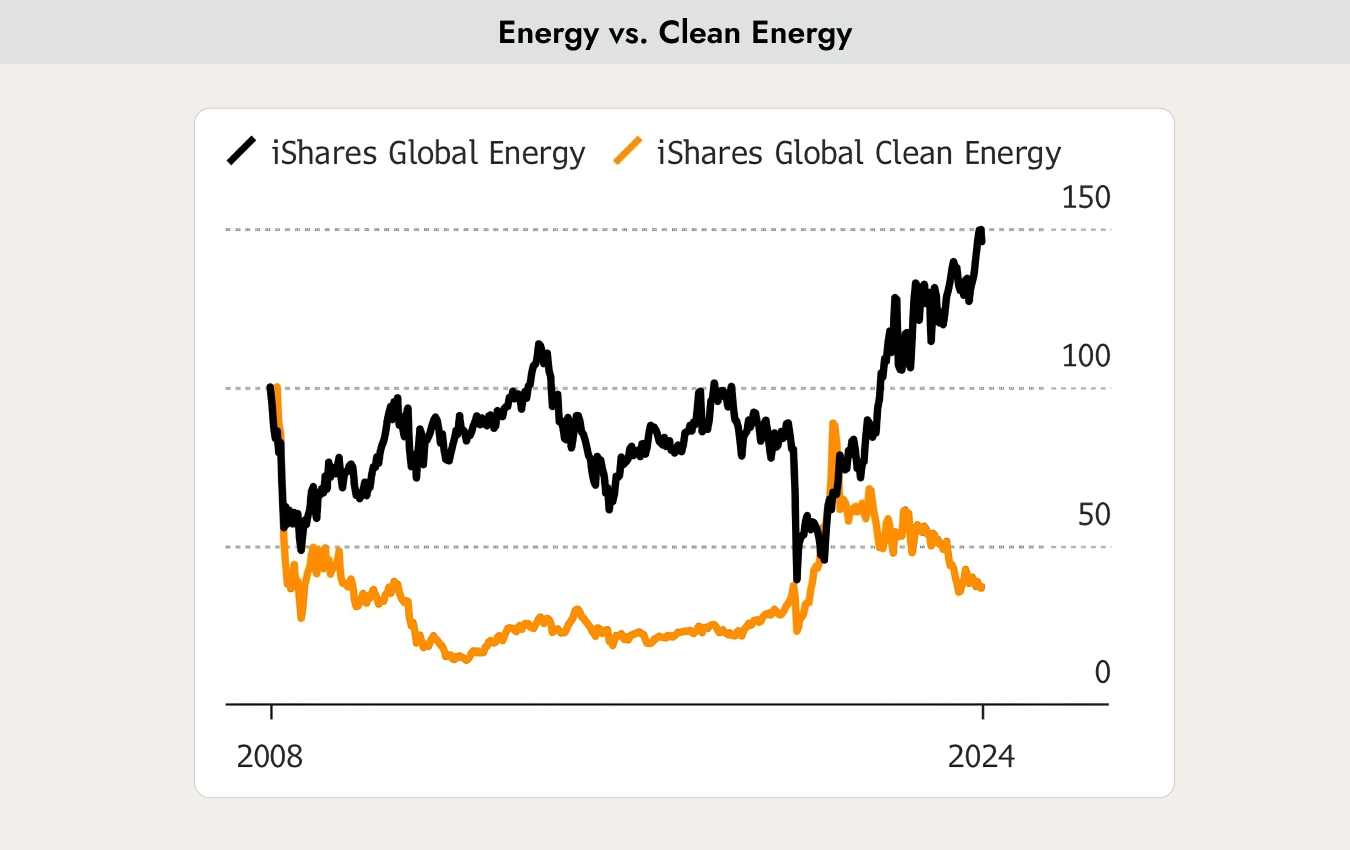

The chart shows the performance of the iShares Global Energy and iShares Global Clean Energy ETFs. While the iShares Global Energy ETF (black line) has delivered overall positive performance since 2008, the iShares Global Clean Energy ETF (orange line) has shown much more volatility. Since 2020, however, global energy stocks have experienced a significant rise, while clean energy stocks, after a strong rally, have since declined again.

How is it possible that everyone is talking about the energy transition, yet investors who put money into companies in this sector are losing money?

This was due to two factors:

- Solar panels and wind turbines have become increasingly cheaper, and many new facilities are being installed. At the same time, however, destructive competition emerged. China identified the new energy sector as strategically important. Rare earth materials — 90% of which come from China and are used in solar panels and batteries — were intended to be processed locally rather than exported. Through hidden subsidies, Chinese solar panel manufacturers rose to market leadership. U.S. and European companies, burdened by higher cost structures, had little chance to compete and went bankrupt in large numbers or were acquired by Chinese firms. In the battery sector, this displacement competition is still in full swing, and in electric vehicles, it has only just begun. Both industries face the same fate as solar panel manufacturers. Consumers benefit from falling prices, and globally, the energy transition may accelerate as a result — but at the cost of near-total dependence on China.

- Many companies in the new energy sector are smaller firms developing emerging technologies. They rely on government subsidies or access to low-interest financing. COVID led many governments to reallocate funding priorities, while the unprecedented rise in interest rates since 2021 resulted in sharply higher financing costs. Both factors have been toxic for smaller companies focused primarily on growth.

Despite all the enthusiasm and optimism surrounding new energy, investors should avoid investing blindly. Instead, they should closely monitor global economic developments and critically assess how these trends may impact the sector from an investment perspective.

We, too, were caught up in the enthusiasm surrounding this theme and invested enthusiastically. When the first losses appeared, we reassessed the market and were able to exit in time before prices declined significantly further.

The sector remains interesting and may continue to offer investment opportunities. However, from our perspective, the right time may come only once interest rates begin to decline. This is likely to happen toward the end of the year.

In addition, we advise against ETFs in this space and would instead favor active fund managers. They are better positioned to invest in companies that are least affected by the destructive price competition driven by China.

Outlook for Tesla and NVIDIA

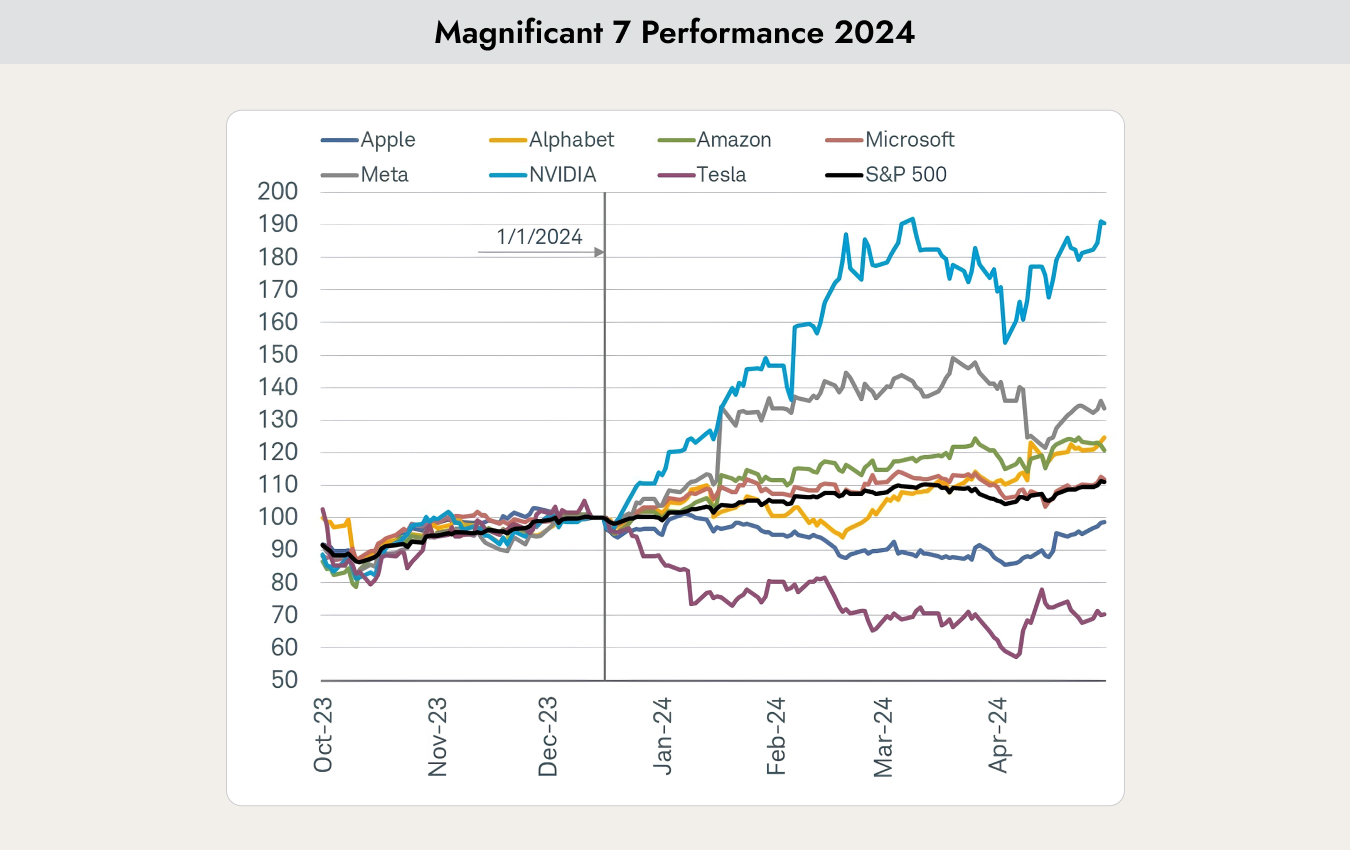

Last year, nearly 70% of the gains in the S&P 500 came from just seven stocks — the “Magnificent 7” (Apple, Google, Amazon, Microsoft, Meta, NVIDIA, and Tesla). This year as well, the majority of these stocks have performed positively, though not all. It is time to take a closer look at the best-performing stock (NVIDIA) and the worst-performing one (Tesla).

The chart shows the stock price performance of the Magnificent 7 compared to the S&P 500. NVIDIA gained another 190% this year, while Tesla declined by 30–40%.

There are two fundamental investment strategies that contradict each other:

- The Trend Is Your Friend: This is one of the best-known sayings in investing. Trends often last longer and go further than most people expect. Had investors sold Apple shortly after the success of the iPhone, they would have missed the biggest gains — the same applies to Google and Amazon.

- Value Investing Based on Valuation: This strategy is primarily based on valuation. A stock is purchased when it can be bought at a discount of at least 20% to its intrinsic value. If the stock becomes overvalued, it is sold.

The key question surrounding the Magnificent 7 is: when is enough, enough? On average, stocks with a P/E ratio above 25 are considered expensive. The current P/E ratios of the Magnificent 7 are as follows: Meta, Google, Microsoft, and Apple range between 25 and 40. Tesla has a P/E ratio of 86, NVIDIA stands at 250, and Amazon at 312.

A P/E ratio of 250 means that if you were to buy the entire company today, the company would need to generate the same level of profit as it does now for 250 years before you would earn back your investment. Only in year 251 would the purchase be fully paid off.

Since stock market indices have not even existed for 250 years, let us use Tesla, with a P/E ratio of 86, for the next comparison. If we look at the S&P 500, only 30 of today’s 500 companies existed 86 years ago. Making forecasts over such a long period is like reading tea leaves.

However, all of these arguments from value investors could already have been made at the end of 2023, when NVIDIA’s P/E ratio stood at 50. Had investors sold at that point, they would have missed out on the 190% gain this year. So the question remains: when is enough, enough? How long should investors stay invested, and when is the right time to exit?

When investing in stocks such as the Magnificent 7, it is essential to analyze the underlying trend and form an opinion on whether it is likely to continue. Investors must also consider whether the broader economic environment still supports that trend.

Tesla:

Underlying trend: electric mobility (cars), energy transition (batteries).

Anyone who has read the market report from the beginning already knows the answer. The underlying trends that drove the success have changed significantly.

Government subsidies are being gradually reduced. In Germany, the €4,000 subsidy per electric vehicle was abolished at the end of 2023. In Switzerland, electric vehicles have also been subject to taxes since 2024.

China has identified both the electric vehicle and battery sectors as strategically important. The Chinese company BYD (Build Your Dreams) is now the world’s largest manufacturer of electric vehicles and is beginning to expand into the U.S. and European markets.

We do not want to be misunderstood here. We are not predicting Tesla’s bankruptcy. Tesla is a strong and innovative company that is, and will remain, an important market player in many areas. However, the magic is over, and competition has become brutal.

Tesla may still be a good investment for those seeking short-term gains. Following the latest quarterly earnings and the announcement of 100% import tariffs on BYD vehicles in the U.S., the stock price rose by 50%.

However, we removed Tesla from our long-term portfolio at the beginning of 2024.

NVIDIA

Underlying trend: artificial intelligence.

The chart shows how many companies in the S&P 500 mentioned the term “artificial intelligence” during their first-quarter 2024 earnings calls. Around 41% of companies plan to invest in the sector and adopt tailored AI solutions. The trend remains unbroken.

Developing strong AI solutions usually requires powerful language models as a foundation. Companies such as OpenAI, Meta, and Google have invested enormous effort into building these. For new companies aiming to offer AI solutions, this has traditionally created a high barrier to entry. That was the case until recently — but over the past few weeks, this is no longer necessarily true.

Meta has decided to make its language model, Llama, freely available to developers under an open license. This is a similar move to when Google made its Android operating system open-source. Developers can now begin building new solutions immediately, without major additional costs. However, the computing power required to run these solutions is still offered almost without competition by one company: NVIDIA.

China is also highly active in the artificial intelligence trend. Most patent filings in this field currently come from China. However, China has not yet produced a breakthrough “killer application” in AI. In addition, China does not (yet) possess the expertise to manufacture chips that come close to matching NVIDIA’s capabilities.

Despite the seemingly insane P/E ratio of 250, we remain invested in NVIDIA, which we have held in our long-term equity portfolios since 2020.

NVIDIA will publish its quarterly earnings this Wednesday. If the results disappoint, we plan to use any weakness in the share price as an opportunity to further increase our position.

.webp)

.jpeg)

.jpeg)

.svg)