Trust and foundation structures in Zollikon for wealth protection are defined as legal arrangements that separate family assets from personal ownership, creating a formal barrier between wealth and personal liability. Swiss foundations are governed under Article 335 of the Swiss Civil Code, while trusts operate under foreign law and are recognised in Switzerland through the Hague Convention. Together, these two vehicles form the backbone of serious, multi-generational asset protection for families in Zollikon and the wider Zurich region. Marmot works with families navigating precisely this territory, where the right structure can mean the difference between wealth that endures and wealth that erodes.

What are the key differences between trusts and foundations in Zollikon?

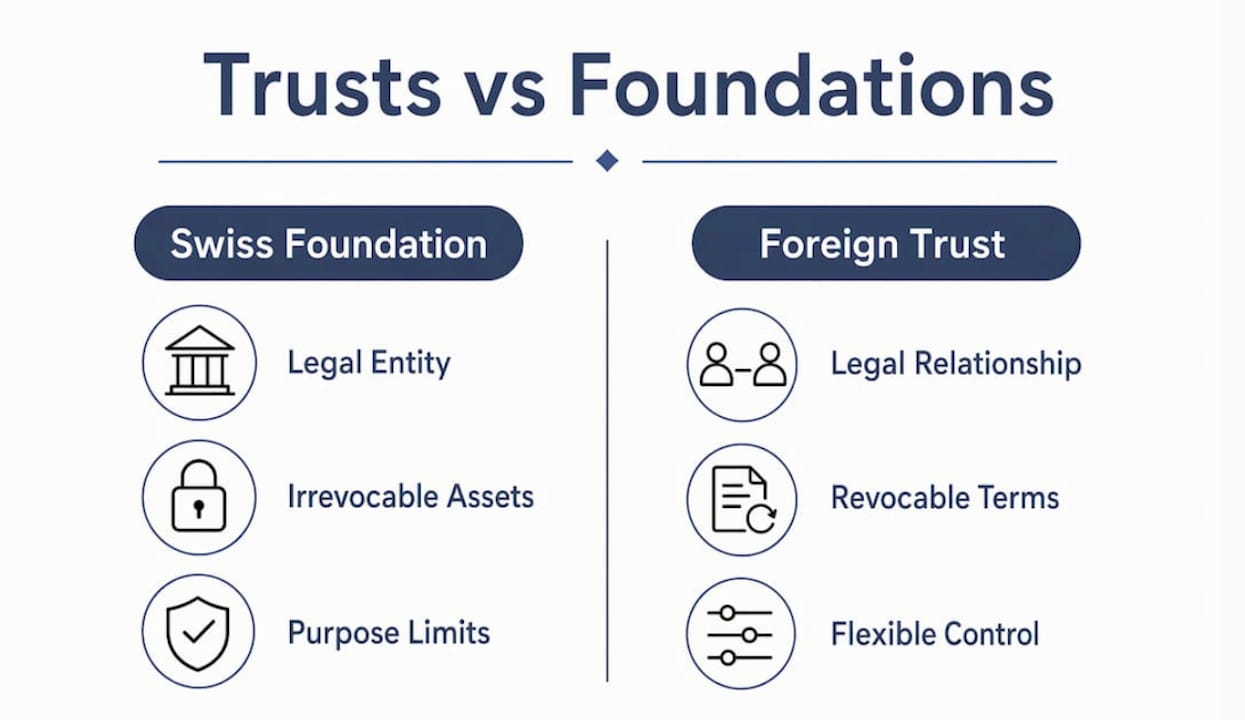

Swiss family foundations are autonomous legal entities governed under Article 335 of the Swiss Civil Code. They are restricted to specific family-support purposes, including education, maintenance, and the raising of family members. A foundation cannot serve as a general wealth accumulation vehicle or function as an unrestricted family bank. All distributions must align with a defined support purpose, and the foundation’s charter must be drafted carefully to avoid nullification.

Trusts, by contrast, are not domestic Swiss legal entities. Swiss law recognises foreign-law trusts under the Hague Convention but has no domestic trust legislation of its own. A trust is a legal relationship in which a settlor transfers assets to a trustee, who manages them for the benefit of named beneficiaries. This structure offers considerably more flexibility than a foundation, particularly for international asset management and discretionary benefit allocations.

The table below summarises the principal differences between the two structures in the Swiss context.

The irrevocability of a foundation is its defining characteristic. Once assets are transferred, they legally belong to the foundation and not the founder. This provides strong protection against personal creditors, though clawback provisions and forced heirship rules under Swiss law can still apply in certain circumstances. Trusts offer more flexibility but require FINMA-authorised trustees to operate legally within Switzerland.

How can these structures be integrated into layered wealth protection strategies?

Layered wealth protection strategies combine foundations, holding companies, and life insurance to create frameworks that protect core family wealth from multiple angles. Hybrid structures are widely used in Zurich and Zollikon, where families often hold significant intergenerational assets across multiple jurisdictions. The separation between foundation assets and an operating holding company prevents business liabilities from reaching the principal family wealth. This separation is critical in multi-entity structuring and is one of the primary reasons families in Zollikon choose this approach.

A practical multi-layered structure for a Zollikon family might be organised as follows:

- Swiss family foundation holds the core intergenerational assets, governed by a defined charter focused on family support and education purposes.

- Holding company sits beneath or alongside the foundation, managing operating investments, real estate, and business interests separately from foundation assets.

- Discretionary trust (governed by Jersey, Liechtenstein, or another recognised jurisdiction) manages international assets and provides flexible benefit allocations to beneficiaries across borders.

- Life insurance wrapper provides liquidity and tax efficiency for specific asset classes, particularly for beneficiaries in high-tax jurisdictions.

- Liquid emergency reserve sits entirely outside formal structures, accessible immediately without disrupting legal arrangements.

Industry guidance recommends holding 3–6 months of living expenses in accessible reserves separate from main wealth structures. This ensures families can meet immediate needs without triggering distributions from a foundation or trust, which may carry tax or governance implications.

Pro Tip: Draft the foundation charter with enough specificity to satisfy Article 335 requirements, but enough breadth to accommodate changing family circumstances over decades. A charter that is too narrow can restrict legitimate distributions; one that is too broad risks nullification.

Typical portfolio allocations across these structures vary by family profile, but the principle remains consistent: no single vehicle should carry all the risk or all the assets. Diversification across legal structures is as important as diversification across asset classes.

What governance and control considerations affect wealth protection?

Excessive control by a founder or settlor is the most common reason wealth protection structures fail to deliver their intended benefits. When a founder retains too much influence over a foundation or trust, courts and tax authorities may treat the assets as still belonging to the founder personally. This undermines both the creditor protection and the tax advantages the structure was designed to provide. Independent governance via foundation boards or professional trustees is not optional; it is the mechanism that makes the protection real.

Effective governance for Zollikon families typically involves several practical commitments:

- Appointing an independent foundation board with at least one member who has no family connection to the founder.

- Establishing a written family governance framework that defines how decisions are made, how disputes are resolved, and how heirs are prepared for their roles.

- Holding regular board meetings with formal minutes, even when no major decisions are required.

- Reviewing the structure’s legal and tax position at least every three years, or whenever Swiss law changes materially.

- Preparing the next generation through structured financial education before they assume governance responsibilities.

Multi-generational wealth preservation requires not only legal tools but also effective family governance and successor preparation. A disciplined governance framework is foundational to maintaining family wealth through market and regulatory changes. Structures that lack this framework tend to fragment within two generations, regardless of how well they were originally designed.

Pro Tip: Treat the family governance framework as a living document. Review it whenever a significant family event occurs, such as a marriage, divorce, birth, or the death of a key family member. Governance that reflects current family reality is far more effective than governance that reflects the family as it was when the structure was first established.

The continuity of wealth management across generations depends on heirs understanding both the purpose and the mechanics of the structures they will one day govern. Preparing heirs for governance roles is as important as the legal structuring itself.

What legal and regulatory factors should Zollikon residents consider?

The legal framework governing trusts and foundations in Switzerland is specific, and Zollikon residents need to understand several key constraints before establishing either structure.

The most significant legal considerations are:

- Article 335 Swiss Civil Code restricts family foundations to education, support, and the raising of family members. A foundation cannot be used for general wealth accumulation or as a perpetual family bank. The charter must reflect a genuine support purpose.

- Hague Convention recognition means Switzerland acknowledges foreign-law trusts but does not provide a domestic trust law. The trust deed must be governed by a recognised foreign jurisdiction, such as Jersey, Liechtenstein, or the Cayman Islands.

- FINMA regulation requires that trustees operating in Switzerland obtain authorisation from the Swiss Financial Market Supervisory Authority. Using an unregulated trustee creates legal and compliance risk.

- Irrevocability of foundation assets means that once assets are endowed, the founder cannot reclaim them. This provides strong creditor protection but demands certainty before transfer. Clawback provisions under Swiss insolvency law can still apply if assets were transferred to defraud creditors.

- Forced heirship rules under Swiss succession law give certain heirs a statutory entitlement to a portion of the estate. Transfers to a foundation or trust do not automatically override these rights, and structures must be designed with this in mind.

Tax-efficient wealth structuring through holding companies alongside foundations can address some of these constraints, but the interaction between cantonal tax rules and federal law requires professional advice specific to Zollikon and the Canton of Zurich. Structures that work efficiently in Zug may need adjustment for Zollikon residents given differences in cantonal tax treatment.

Families should also maintain liquid emergency reserves outside formal structures. Accessing funds from a foundation or trust mid-cycle can trigger tax events or require board approval, neither of which is practical in a genuine emergency.

Key takeaways

Trusts and foundations in Zollikon provide legally distinct but complementary tools for protecting family wealth across generations, and their effectiveness depends on governance as much as legal structure.

Balancing control and protection: a perspective from the field

I have seen families spend considerable time and money establishing a Swiss family foundation, only to undermine it entirely by retaining day-to-day control over every distribution decision. The legal form was correct. The governance was not. Courts and tax authorities look at substance, not structure, and a foundation where the founder effectively runs everything is not a foundation in any meaningful protective sense.

The families who get this right tend to share one characteristic: they accept early that the structure is not about control. It is about continuity. They appoint independent board members who will push back, they document decisions properly, and they treat the foundation as a genuine institution rather than a personal account with extra paperwork.

The hybrid approach, combining a foundation for core governance with a trust for international flexibility and a holding company for operating assets, is the most practical framework I have seen for Zollikon families with complex, multi-jurisdictional wealth. It is not the simplest arrangement, but simplicity is rarely the right goal when the stakes are generational. What matters is that each layer serves a defined purpose, that liquidity is always available outside the formal structures, and that the family understands what they own, why they own it that way, and what happens next.

Seeking professional guidance familiar with both Swiss Civil Code specifics and Zollikon’s cantonal context is not a luxury. It is the foundation of a structure that will actually work when it needs to.

— Sophie Steinmann

How Marmot supports Zollikon families with wealth structuring

Marmot works with families and individuals in Zollikon who are ready to think seriously about how their wealth is held, governed, and passed on. The questions around trusts, foundations, and multi-layered structures are rarely straightforward, and the answers depend heavily on your family’s specific circumstances, tax position, and long-term objectives.

Marmot’s advisers bring direct experience with Swiss family foundations, FINMA-regulated trust arrangements, and the governance frameworks that make these structures work across generations. If you are considering establishing a foundation or trust, or reviewing an existing structure, speak with Marmot’s team to begin a conversation tailored to your situation. The first step is simply understanding what is possible.

FAQ

What is a Swiss family foundation?

A Swiss family foundation is an autonomous legal entity governed under Article 335 of the Swiss Civil Code, established to support family members through education, maintenance, or similar defined purposes. Asset transfers to a foundation are irrevocable, meaning the assets legally belong to the foundation and not the founder.

Does Switzerland have its own trust law?

Switzerland does not have domestic trust legislation. It recognises foreign-law trusts under the Hague Convention, meaning a trust must be governed by a recognised foreign jurisdiction such as Jersey or Liechtenstein, and any trustee operating in Switzerland must hold FINMA authorisation.

Can a foundation protect assets from creditors in Zollikon?

A Swiss foundation provides strong creditor protection because endowed assets legally belong to the foundation rather than the founder. However, Swiss insolvency law includes clawback provisions, and forced heirship rules can still apply, so the structure must be designed with these constraints in mind.

What is the difference between a trust and a foundation for wealth protection?

A foundation is a separate legal entity with strict purpose restrictions and irrevocable asset transfers, making it well suited to long-term governance. A trust is a legal relationship offering greater flexibility for international asset management and discretionary distributions, but it requires a FINMA-regulated trustee to operate in Switzerland.

How much should I keep outside formal wealth structures?

Industry guidance recommends holding 3–6 months of living expenses in liquid reserves entirely separate from foundations or trusts. This ensures immediate access to funds without triggering distributions that may carry tax or governance implications.

Recommended

- Tax-Efficient Wealth Structuring in Switzerland: Investor guide | Marmot Finance

- Wealth Management in Zollikon | Marmot Finance

- Preserving Generational Wealth: Private Wealth Management in Switzerland | Marmot Finance

- The 3rd Pillar: More Than a Fad | Marmot Finance

.webp)

.jpeg)

.svg)