Chart of the Week

The chart shows the global food price index calculated by the UN. Due to the war in Ukraine, food prices have risen sharply and have already returned to the levels seen in 2011, when massive unrest and political upheavals occurred across the Arab world.

Why This Matters

Sharply rising food prices often lead to widespread dissatisfaction in emerging markets. This became evident in 2011, when protests over high food prices triggered unrest around the world.

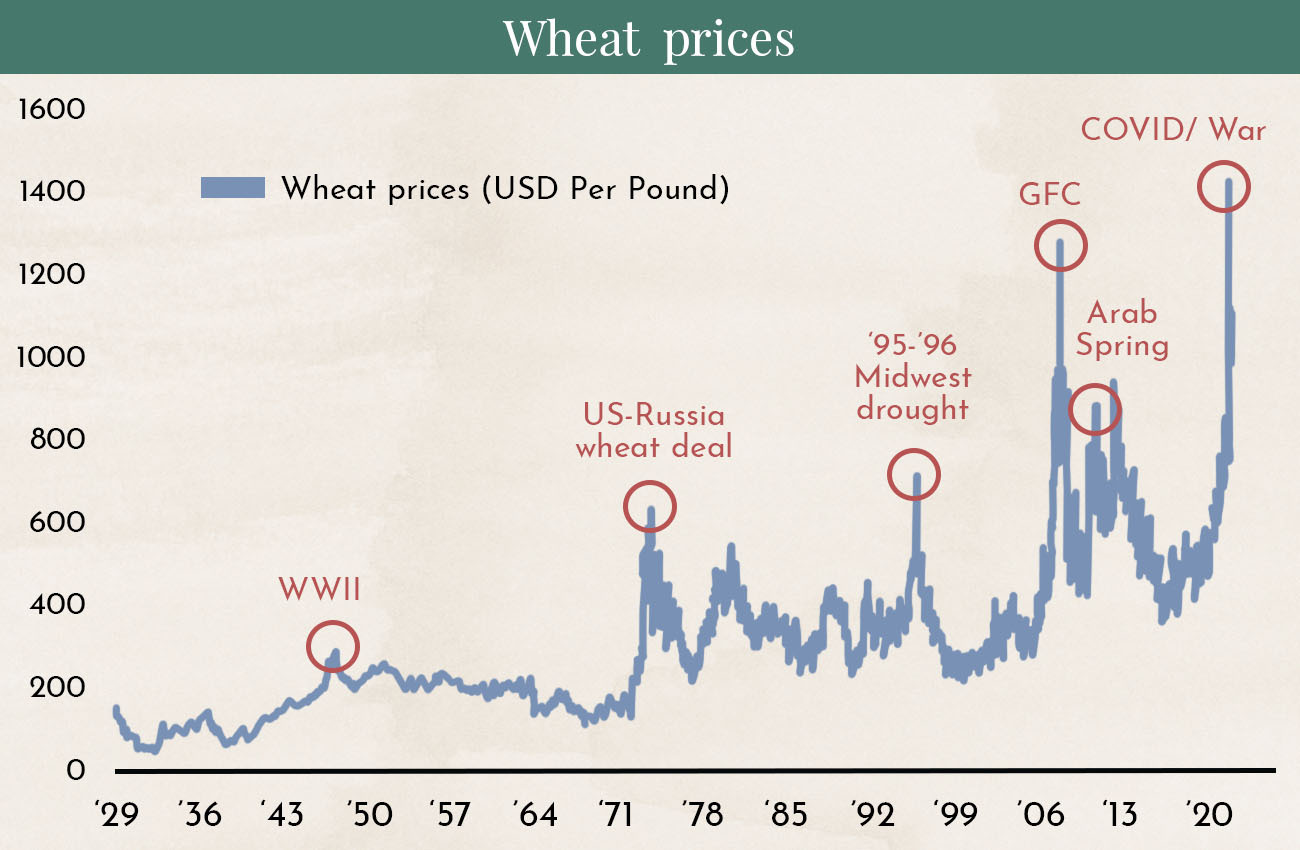

The chart shows the development of wheat prices since 1929. Ukraine is considered the breadbasket of Europe. Due to the war, many agricultural fields have been destroyed. Even after the partial withdrawal of Russian troops from western Ukraine, many fields remain mined, making cultivation possible only to a limited extent. As a result, a decline in wheat prices is not expected immediately, even if the war ends. It will likely take until the end of the year for the situation to normalize.

Persistently high food prices have the potential to trigger political unrest.

Ukraine War: Scenario Analysis

The war in Ukraine has now been ongoing for one and a half months. How much longer will it last, and what are the implications for the financial markets? We see four possible scenarios.

War Ends on May 9, 2022

On May 9, as he does every year, the Russian president will attend the military parade on Red Square and deliver a speech on “Victory Day.” This day commemorates the victory of the Soviet Army over Nazi Germany in World War II.

Declaring victory in Ukraine would fit well with the occasion. However, we believe that by then, Russia will not have captured enough additional territory to present the war as a victory.

Probability: 10%

War Ends in 3 Months — June 2022:

Military experts consider it realistic that Russia may need three months to bring eastern and southern Ukraine under its control. If Odessa were also to fall, this would be an additional bonus. Putin could easily portray the war as a victory, with many additional territories under his control.

However, the original war objectives — destroying the Ukrainian army, “denazifying” Ukraine, and removing the government — would still not have been achieved. In this context, the capture of Mariupol and victory over the Azov Battalion are particularly important.

The Azov Battalion is a coalition of right-wing nationalist militia units that have been accused of numerous human rights violations and war crimes since 2014. These actions form the basis of Russia’s propaganda narrative that it seeks to “liberate” Ukraine. If this unit were to fall, Russia could present it as a victory and as the fulfillment of its war objectives.

Probability: 50%

War Ends in 6 Months — September 2022:

The big question is where Putin will stop his campaign of conquest. If he secures lasting control over eastern and southern Ukraine, he may be tempted to push further from a position of strength and attempt to achieve the original war objectives by conquering all of Ukraine.

This is particularly problematic because the West would then likely have to impose the same sanctions on Ukraine as on Russia in order to prevent sanctions circumvention. The return of refugees from Ukraine would no longer be possible for years.

Probability: 35%

War Between Russia and the Entire NATO Alliance

Due to the extensive weapons deliveries, Putin already has sufficient grounds to expand the war to the entire NATO alliance. Such an escalation would have devastating consequences for both Europe and Russia.

We do not believe such an escalation is likely, but a combination of miscalculations and mistakes by political leaders in NATO countries, as well as in Russia, could lead to such an outcome.

Probability: 5%

Impact on the Economy and Financial Markets

For now, we will limit our analysis to our main scenario: the war ending within three months. The Russian economy is primarily linked to the economies of Europe and the United States through the energy sector (oil and gas) as well as raw materials such as nickel, palladium, and copper.

Oil and gas prices collapsed sharply after the first COVID lockdowns in March 2020, but then already doubled in price afterward. This enormous base effect had a major impact on inflation in both the United States and Europe. Following the outbreak of the war in Ukraine, prices rose again. However, this increase has already been contained through the release of strategic reserves.

We expect that the worst is already behind us. Inflation has therefore likely reached its peak levels for now.

One major consequence could be Europe abandoning all Russian energy supplies. However, at present, it is expected that Europe will only take this step if alternative sources are available. These alternatives could come from Iran or Venezuela.

A peace agreement after three months will only be possible if the West is also involved. There would need to be a demilitarized zone monitored by the UN, and some of the sanctions against Russia would likely have to be lifted. This may not be politically popular at the moment, but it is the only way a lasting peace could be achieved. Such a development would have a calming effect on the financial markets.

The chart shows a monthly survey conducted by the Bank of America among the world’s largest asset managers regarding where they see the biggest risks. What is remarkable is the decline in concerns about the war in Ukraine, which supports our scenario analysis. From a market perspective, the war already appears to be over, and the financial markets are once again focusing on the medium- and long-term economic outlook, with steadily rising interest rates. At the same time, fears of a global recession are increasing, along with concerns that central banks may raise interest rates too aggressively.

The chart comes from the same Bank of America survey cited above. The majority of the world’s largest asset managers expect lower inflation figures in the coming months. This also supports our scenario analysis.

Is Bitcoin on the Verge of the Next Major Rally?

Since the outbreak of the war in Ukraine, Bitcoin has gained 5% in value. At times, the increase even reached 25%, but the ongoing regulatory debate in the United States — and especially in Europe — has led to a correction. Now, however, there are growing signs that Bitcoin could be preparing for a new upward move.

The chart shows how the different investor groups are behaving. The key factor for a price increase is whether the very large investors — the so-called whales — begin buying (red dots). This was the foundation for major price rallies in November 2020, August 2021, and February 2021 (black circles in the chart). For the past two weeks, we have once again seen whales buying.

The risks, however, remain high. A group of members of the European Parliament managed to introduce a provision into draft legislation that would effectively ban private wallets on anti-money laundering grounds. The background to this is the EU regulatory proposals Markets in Crypto-Assets (MiCA) and the Transfer of Funds Regulation (TFR), both of which have been heavily criticized by the crypto industry. A ban on private wallets would effectively amount to a ban on Bitcoin in Europe. It is to be hoped that Parliament will further educate itself on the issue and recognize the consequences such a provision could have. An open letter from the European crypto community to policymakers in Parliament will hopefully be heard.

A month earlier, a minority within the committee had already attempted to introduce an article that would have allowed only “sustainable” cryptocurrencies. Since Bitcoin operates using the Proof-of-Work mechanism, which requires a large amount of energy, this would effectively have meant a ban on Bitcoin and all cryptocurrencies based on the same system. Other cryptocurrencies, however, would not have been affected. This proposed article was successfully rejected.

Disclaimer:

The content in these blogs is provided solely for general informational purposes and is intended to help potential clients gain an understanding of how we work. It does not constitute recommendations to buy or sell assets and should not be considered investment advice. Marmot.Finance cannot assess whether or how the statements made align with your investment objectives or risk profile. If you make investment decisions based on this blog post, you do so entirely at your own risk and responsibility. Marmot.Finance cannot be held liable for any losses that may arise from the information contained in this blog post. The products mentioned are not recommendations, but are intended to demonstrate how Marmot.Finance works and selects such products. Marmot.Finance is also completely independent and does not earn compensation of any kind from product providers.

.webp)

.jpeg)

.jpeg)

.svg)