Chart of the Week

The chart shows the size of the balance sheets of the central banks of the United States, Europe, Japan, and China. In particular, the European Central Bank (ECB, blue) and the US Federal Reserve (FED, red) significantly expanded their balance sheets during the pandemic period.

Why This Matters:

To protect the economy from more severe consequences, central banks sharply reduced interest rates and expanded their balance sheets. The balance sheets were increased primarily through the purchase of bonds on the market, but also through very low-interest loans to commercial banks. This support for the economy is also referred to as loose (or in this case, ultra-loose) monetary policy.

US Federal Reserve Tightens the Screws.

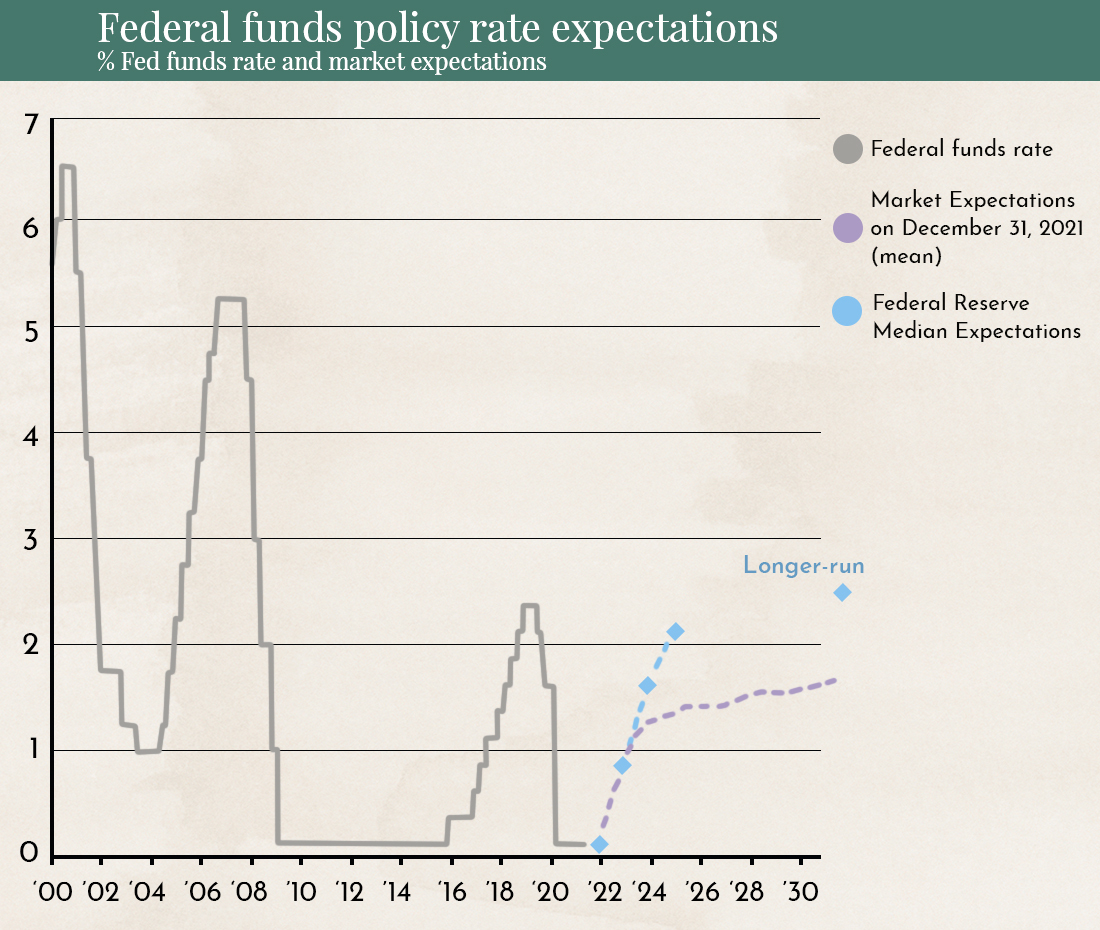

The era of ultra-loose monetary policy is now over. In December, the US Federal Reserve announced that it would significantly reduce the expansion of its balance sheet and end bond purchases by the end of March. At the time, it had been expected that the central bank would continue these purchases until June 2022. Meanwhile, most market participants expect 2–3 interest rate hikes by the end of 2022:

This week brought the next major shock. The minutes from the US Federal Reserve’s December meeting were released, revealing that not only will bond purchases be ended, but the balance sheet itself is also expected to be reduced. This would represent a shift from an (ultra) loose monetary policy to a restrictive one within just a few months. Even the more pessimistic market participants had not expected this until the end of 2022. As a result, equity markets corrected downward accordingly.

A shift from loose to restrictive monetary policy by the US Federal Reserve also requires an adjustment in investment strategy across most portfolios. It is also likely that the European Central Bank will soon take a similar step.

Annual Outlook

Normally, readers expect clear forecasts under this heading about how the stock market will perform in the coming year. We usually provide such forecasts as well, but in the current pandemic environment, everything is different. In 2020 and 2021, central banks intervened in the financial markets more heavily than ever before. On top of that came the generous government support packages.

This led to most governments accumulating debt on a scale normally seen only after a world war.

The chart shows the level of government debt relative to gross domestic product (GDP) for developed countries (blue) and developing countries (red). Debt levels are now higher than they were after the Second World War.

Various studies also show that around one-third of all Covid support funds flowed into the financial markets, which was one of the main reasons for the very strong performance across nearly all markets in 2021.

Our forecast is that society will learn to live with COVID. In 2022, central banks will end their ultra-loose monetary policy and begin raising interest rates. Governments will also start reclaiming the loans granted during the crisis. So far, we are seeing unusually strong economic growth, and it is possible that the economy can withstand these tightening measures without major damage — but only if central banks and governments manage the transition wisely and gradually.

And that is precisely why reliable forecasts are currently not possible. Central banks act in a relatively coordinated manner and consult with the central banks of other countries, even if they occasionally pursue their own path. Governments, however, are different. Political majorities can lead to decisions that are neither coordinated with other countries nor with central banks. Predicting which country will respond wisely is therefore almost impossible. Government measures have the potential to trigger a crash in the financial markets.

As a result, market volatility in 2022 is expected to be higher than in 2021. Investors may need to adjust their investment strategy several times throughout the year and remain flexible in adapting their portfolios.

2020 and 2021 were the years of new digital business models. At times, the stocks of these companies gained more than 300%.

The chart shows an index created by Goldman Sachs that includes technology companies with innovative business models that have never generated a profit. These include well-known companies such as Uber, Pinterest, Spotify, and Slack.

We believe in the comeback of quality stocks. These are companies with proven business models that have generated strong profits for many years. The outlook for companies selling little more than hype and promises is likely to become much more challenging. Until now, capital to finance their losses was easily available and almost free. With interest rates now rising, that financing will become increasingly difficult.

One of the most important factors — and a key foundation for central bank policy — will be inflation:

The chart shows how sharply inflation increased in 2021, but also that most market participants expect inflation to decline significantly again in 2022. We are more skeptical. Supply chains remain heavily disrupted:

The chart shows a JPMorgan index that measures delivery times. The lower the index, the longer the delays. A slight recovery is in sight, but it will likely take at least another year before supply chains return to normal.

An equally important factor for inflation is unemployment — when unemployment is low, wages tend to rise:

The chart shows unemployment (purple) and the number of open jobs in millions in the United States. The number of job openings is now higher than the number of unemployed people. In addition, many job seekers lack some of the qualifications required for the available positions.

Due to the ongoing supply chain issues and the labor market situation in the United States, we currently expect inflation to remain higher than most market participants anticipate.

There are two main ways to protect against high inflation: investing in real assets and gold. For a liquid portfolio, equities are the most prominent real assets. In such a scenario, bond exposure should be kept as low as possible.

For equity investments, we favor quality stocks and value companies. Firms that are market leaders in a sector or niche are also better positioned to raise prices if inflation persists.

The chart shows the sector weightings in the country indices (top) and in the value/growth indices (bottom).

To implement the strategy outlined above — with less emphasis on technology and greater exposure to consumer and industrial companies — the US equity market should be relatively underweighted, while the European equity market should be overweighted. In addition, we see more attractive opportunities in value rather than growth stocks. One challenge within value indices is their high exposure to banks. We will therefore look for value strategies that maintain a lower weighting in the banking sector.

Disclaimer:

The content in these blogs is intended solely for general informational purposes and to help potential clients gain an understanding of how we work. They do not constitute recommendations to buy or sell assets and should not be considered investment advice. Marmot Finance cannot assess whether or how the statements made align with your investment objectives or risk profile. If you make investment decisions based on this blog post, you do so entirely at your own risk and responsibility. Marmot Finance cannot be held liable for any losses that may arise from the information contained in this blog post.

The products mentioned are not recommendations, but are intended to demonstrate how Marmot Finance works and selects such products. In addition, Marmot Finance is completely independent and does not earn any compensation from product providers in any form.

.webp)

.jpeg)

.jpeg)

.svg)